Markets often frame oil as a direct driver of equity performance, with rising prices assumed to pressure stocks and falling prices seen as supportive. However, when examined through daily price action across geopolitical events, the relationship appears far less stable and far more dependent on timing and context.

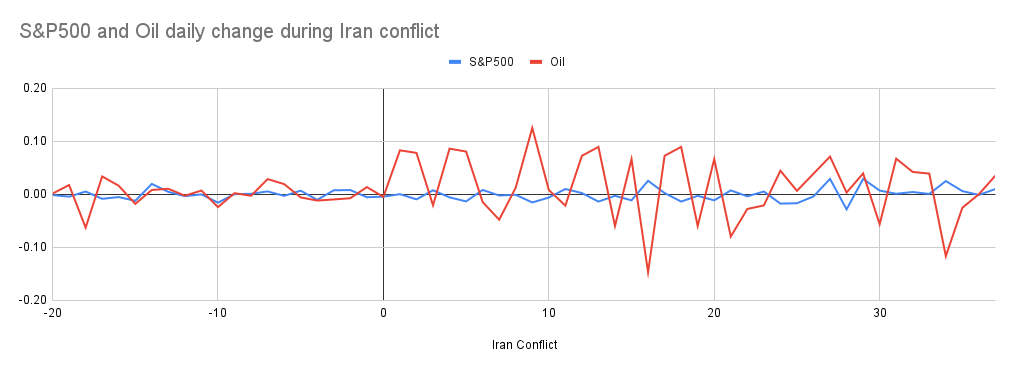

Looking at recent data, plotting daily returns for both the S&P 500 and oil prices around the current geopolitical regime highlights a clear imbalance. Oil exhibits significantly higher volatility, with frequent moves of 5–10% or more, while equity movements remain comparatively contained. This alone explains why simple comparisons often fail. Oil does not move in line with equities, it moves faster and with greater magnitude, dominating any direct relationship.

More importantly, the interaction between the two is not consistent.

In the early phase of the current event, sharp upward moves in oil coincide with periods of equity weakness. This aligns with the conventional narrative. Rapid increases in oil prices act as a proxy for rising geopolitical risk and inflationary pressure, triggering a repricing across equity markets. In this phase, oil functions as a signal, and equities respond accordingly.

However, this relationship begins to fade.

As the timeline progresses, oil remains volatile, but the S&P 500 stabilises. Equity movements become less reactive, even as oil continues to swing. There are periods where oil rises sharply without a corresponding decline in equities, and others where oil falls without triggering a meaningful equity response. The linkage weakens, despite continued instability in the underlying commodity.

This shift is critical.

It suggests that equities are not responding to the level of oil prices, but to the change in regime. The initial spike forces a repricing of risk, but once that adjustment has occurred, markets begin to absorb the information. From that point forward, oil becomes part of the background rather than the primary driver.

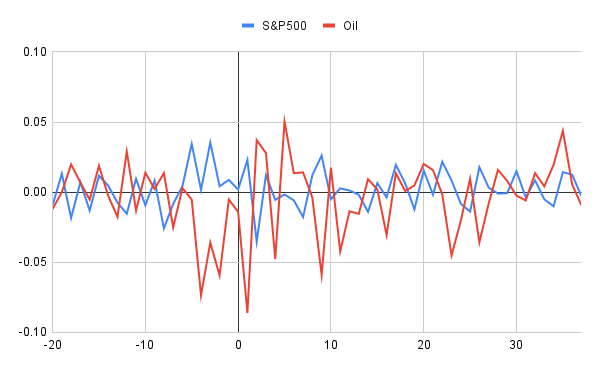

However, this is not a universal outcome. Historical comparisons, particularly with the Iraq conflict, show a different pattern. In that environment, daily price action reflects a more sustained relationship between oil and equities. Movements in oil prices were more consistently mirrored in equity performance, with rising oil aligning more frequently with equity weakness, and declines in oil providing relief. The relationship remained intact for longer, rather than fading after the initial shock.

This distinction highlights an important nuance.

The impact of oil on equities depends on the nature and duration of the underlying shock. And how the market perceives the risk of the event.

When oil price movements are perceived as temporary, typically driven by short-term geopolitical uncertainty, markets adjust quickly. The initial repricing is sharp, but the relationship weakens as stability returns. In these environments, oil acts primarily as a trigger.

In contrast, when oil remains elevated due to sustained supply constraints or prolonged geopolitical tension, it becomes a persistent macro factor. Higher energy costs act as an ongoing drag on growth, margins, and consumption. In these cases, the relationship between oil and equities becomes more durable, with markets remaining sensitive to continued price movements.

This framework helps explain why attempts to establish a stable correlation between oil and equity markets often produce inconsistent results. The relationship is not constant, it is conditional.

In the current environment, the data suggests that markets have largely moved beyond the initial shock phase. While oil remains volatile, equities are showing reduced sensitivity to individual price moves, indicating that much of the immediate repricing has already taken place. However, the risk remains that if oil prices move into a more sustained elevated regime, the relationship could reassert itself.

Looking ahead, the key variable is not the absolute level of oil, but whether the market perceives current price movements as temporary or structural. A renewed sharp spike would likely trigger another phase of repricing. Equally, a prolonged period of elevated prices could shift oil from a short-term signal into a longer-term constraint.

In this context, oil is best understood not as a constant driver of markets, but as a variable whose influence changes depending on the environment.

It does not determine direction. It defines when direction is reassessed, and whether that reassessment is temporary or sustained.