U.S. equities continued their march higher on Tuesday, with all three major indices closing at or near fresh record highs. While the headline gains were modest, the session revealed an interesting shift beneath the surface as investors rotated away from some of the market’s largest technology winners and into industrials, materials and cyclical businesses.

The S&P 500 rose 9.82 points, or 0.13%, to close at a new all-time high of 7,609.78. The index traded between 7,582.99 and 7,620.90 during the session, with the intraday peak marking a new 52-week high. Despite the positive close, leadership broadened beyond the technology sector that has dominated much of 2026’s rally.

The Dow Jones Industrial Average outperformed, gaining 228.91 points, or 0.45%, to finish at a record 51,307.79. Strength in industrials, materials and infrastructure-related companies drove much of the advance. Cisco Systems climbed 5.52%, Caterpillar surged 5.19%, and Apple added 2.88%, helping push the blue-chip index to fresh highs.

Meanwhile, the Nasdaq Composite barely moved, adding just 7.09 points, or 0.03%, to close at 27,093.90. The muted performance reflected profit-taking in several large-cap technology names despite the index itself remaining near record territory. Microsoft fell 4.18%, while investors also rotated away from several recent growth leaders.

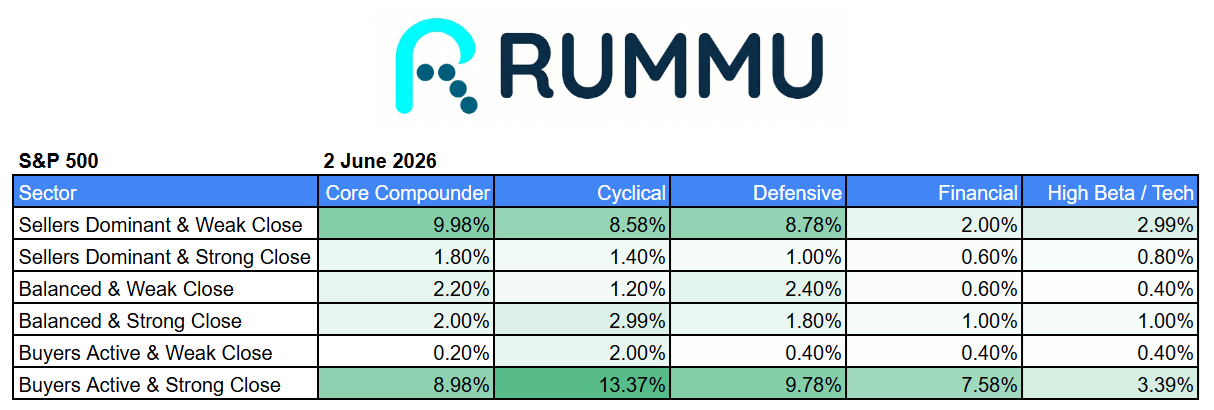

RUMMU’s intraday market data highlighted this divergence clearly. Cyclical stocks showed the strongest buying activity, with 13.37% of names finishing in the “Buyers Active & Strong Close” category. Defensive sectors also displayed notable resilience, with nearly 10% of stocks closing strongly despite broader market leadership rotating away from traditional safe havens.

Core Compounders remained balanced, with strong buying activity offset by continued selling pressure in parts of the group. Financials also quietly improved, posting one of their strongest buyer participation readings in recent weeks as investors broadened exposure beyond technology.

Among the S&P 500’s biggest gainers, Alexandria Real Estate Equities rose 8.50%, Corning gained 7.45%, and networking specialist Ciena advanced 7.44%. Aptiv climbed 7.03% as automotive technology stocks benefited from renewed investor interest, while Axon Enterprise gained 6.40%, continuing its impressive momentum throughout 2026.

On the downside, exchange operators and speculative growth names experienced profit-taking. Cboe Global Markets fell 7.42%, while Copart declined 3.53%. Carvana slipped 3.26% after its recent rally, and Centene lost 3.09%. CME Group also weakened, falling 3.08%.

The sector rotation occurring beneath the surface may be more significant than the index gains themselves. After months of AI-driven technology leadership, investors appear increasingly willing to broaden exposure into industrial businesses, infrastructure providers and economically sensitive sectors. This was evident in the Dow’s outperformance and the strong intraday readings across cyclical industries.

At the same time, the market remains far from defensive. The strong buyer participation in cyclicals suggests investors continue to position for economic resilience rather than slowdown. While technology remains a major driver of overall market performance, Tuesday’s session demonstrated that leadership may be widening beyond the narrow group of AI beneficiaries that have dominated headlines for much of the year.

The result is a healthier-looking market structure. Record highs are increasingly being supported by broader participation rather than relying solely on a handful of mega-cap technology companies. Whether this rotation continues will be one of the key themes to watch as the market moves deeper into the second half of 2026.

For now, investors remain firmly in risk-on mode, with fresh highs across the S&P 500, Dow Jones and Nasdaq reflecting continued confidence in both corporate earnings and the broader economic outlook.