Markets traded with a more constructive tone yesterday, though the strength at the index level masks a still uneven and selective underlying structure. The S&P 500 closed at 7,165.08, up 0.80%, while the Nasdaq Composite outperformed with a 1.63% gain to 24,836.60. In contrast, the Dow Jones Industrial Average lagged, finishing down 0.16% at 49,230.71, highlighting a clear divergence between growth and more traditional, price-weighted components.

This divergence is reflected clearly in the underlying sector behaviour. Technology and growth-led segments provided the primary support, with semiconductors (+1.18%), software (+0.95%), and broader AI-linked areas showing resilience. This aligns with the continued strength seen in higher-level data, where the Nasdaq led gains, driven by sustained demand in technology and AI infrastructure.

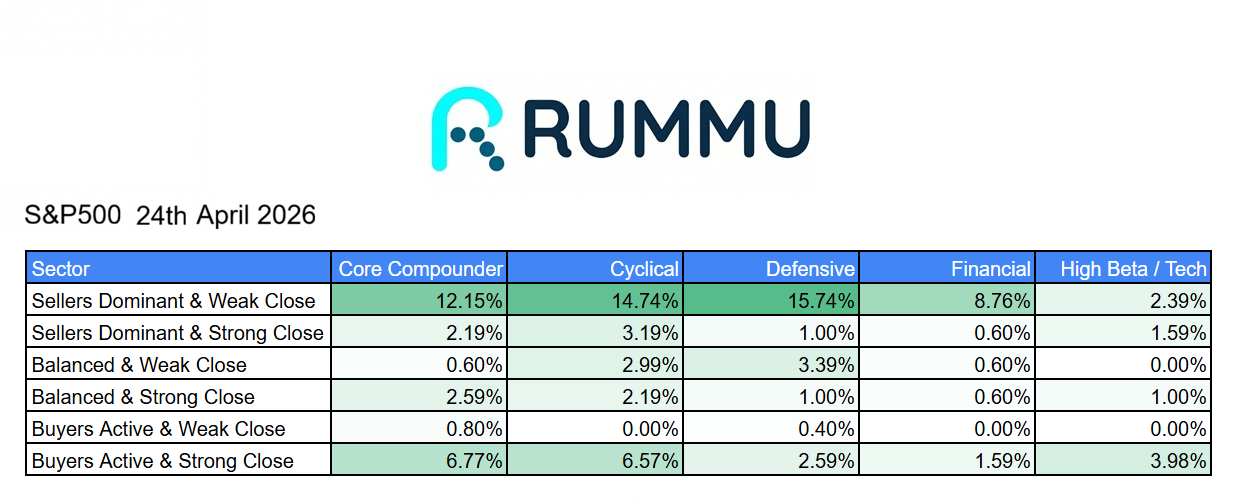

However, this strength was far from broad-based.

Breadth data shows that sellers remained active across much of the market. Core compounders saw 12.15% of stocks classified as “sellers dominant with a weak close,” while cyclicals and defensives were even weaker, at 14.74% and 15.74% respectively. This suggests that despite positive index moves, a significant portion of the market continued to trade under pressure, reinforcing the idea that this was not a fully coordinated rally.

At the same time, there was meaningful, but selective, buyer participation. Around 6.77% of core compounders and 6.57% of cyclicals finished as “buyers active with a strong close,” indicating that demand is present, but concentrated rather than widespread. Defensive participation remained more limited, with only 2.59% of names showing strong closes, highlighting the lack of a broad risk-off rotation.

Sector dispersion further reinforces this mixed picture. Pockets of strength emerged in areas such as networking (+1.35%), consumer technology (+1.48%), cybersecurity (+1.25%), and cloud/SaaS (+1.05%), suggesting continued interest in infrastructure and digital platforms. Materials technology (+2.37%) and electronics (+1.12%) also performed well, indicating selective support in supply chain-linked segments.

In contrast, weakness remained concentrated in several key areas. Telecom was a notable laggard, falling sharply by 6.78%, while biotech declined 4.96%, and media and marketplace segments also remained under pressure. Financials were mixed to weaker, with banking (-1.55%) and broader financial infrastructure declining, highlighting continued sensitivity to macro conditions.

This divergence suggests that while capital is flowing back into growth and technology, it is doing so selectively, rather than signalling a broad risk-on environment.

Importantly, the divergence between the Nasdaq and Dow reinforces this dynamic. Growth-led, capital-light technology continues to attract flows, while more traditional, economically sensitive components remain constrained. This suggests that macro uncertainty has not fully dissipated, but is being selectively bypassed in areas with clearer long-term demand visibility.

Looking ahead, the key question is whether participation broadens.

If strength remains concentrated in a narrow group of technology and AI-linked names, the market may continue to grind higher, but with increasing fragility. However, a rotation into cyclicals, financials, and defensives would indicate a more durable and balanced recovery.

For now, the market appears to be advancing, but not evenly. It is being led, not lifted.