U.S. equities closed mixed on May 8 as investors continued rotating aggressively beneath the surface, even as the headline indices pushed toward fresh highs.

The S&P 500 Index closed at a new record high of 7,398.93, rising 61.82 points (+0.84%) and trading in a relatively tight intraday range between 7,362.97 and 7,401.50. The move extended what has been a powerful momentum-driven rally, with the index now up more than 30% over the past 12 months. Leadership remained concentrated in growth and technology names as investors continued rewarding companies with stronger earnings visibility and AI-linked narratives.

The NASDAQ Composite significantly outperformed, climbing 440.88 points (+1.71%) to close at 26,247.08, marking another record high. The index briefly touched 26,248.62 intraday and has now gained more than 46% over the past year, highlighting the continued concentration of market performance within large-cap growth stocks. The strength in technology continues to reflect investor appetite for businesses with durable earnings growth and structural exposure to artificial intelligence infrastructure spending.

The Dow Jones Industrial Average moved in the opposite direction, falling 313.62 points (-0.63%) to close at 49,596.97 following a volatile session. The Dow had recently pushed above the 50,000 level, but cyclical and industrial names faced pressure as oil prices moved above $100 per barrel amid rising geopolitical tensions in the Middle East. Higher energy prices introduced concerns around inflation persistence and margin pressure across more economically sensitive sectors.

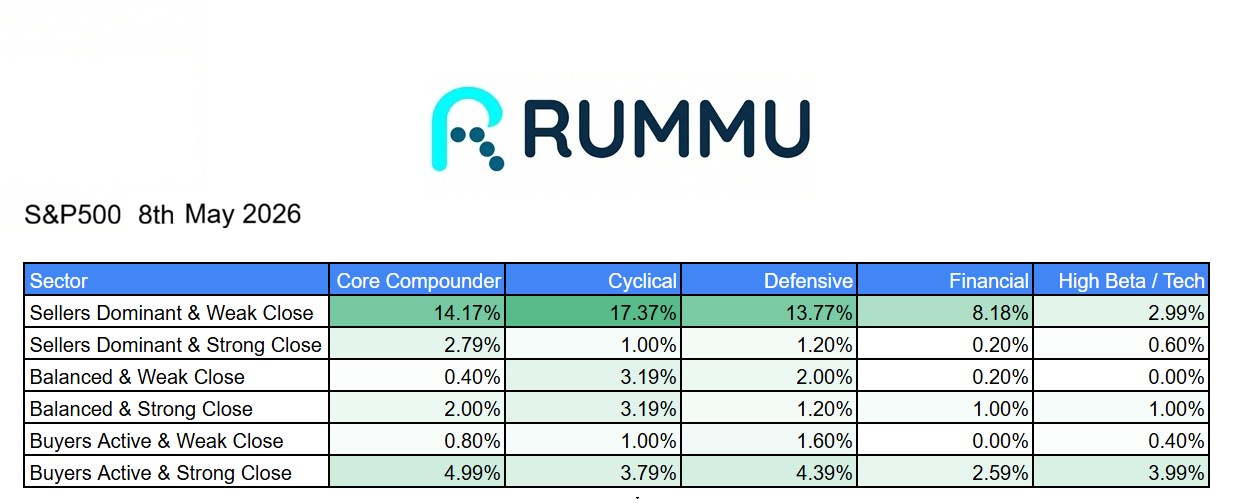

What stood out most during the session was the internal market positioning shown in your sector heat map. Cyclical stocks recorded the highest level of “Sellers Dominant & Weak Close” activity at 17.37%, followed by Core Compounders at 14.17% and Defensive names at 13.77%. This suggests that despite the strong headline performance in the broader market, there was meaningful selling pressure across large portions of the market into the close.

Financials showed significantly lower selling pressure at 8.18%, while High Beta and Technology names saw just 2.99% of stocks close under heavy selling pressure. That divergence helps explain why the NASDAQ Composite continued to outperform. Capital continues flowing toward higher-growth technology names while investors reduce exposure to more cyclical areas that are vulnerable to slowing economic growth and higher commodity prices.

Buyers were active across several sectors, but conviction remained relatively muted. Core Compounders posted 4.99% of stocks in the “Buyers Active & Strong Close” category, while High Beta and Technology names came in at 3.99%. Defensive sectors also showed some resilience at 4.39%, suggesting investors are balancing growth exposure with selective defensive positioning.

The broader takeaway from the session is that headline index strength is masking a more fragmented market underneath. The S&P 500 Index and NASDAQ Composite continue to print new highs, but sector participation remains uneven. Technology leadership remains dominant, while cyclical sectors are beginning to show signs of fatigue as higher oil prices and geopolitical risks create new uncertainty.

For investors, this continues to look like a market being driven by narrow leadership rather than broad participation. As long as earnings momentum in mega-cap technology remains intact, indices may continue grinding higher. However, weakening breadth beneath the surface is becoming increasingly difficult to ignore.