Markets traded with a weaker and more rotational tone yesterday, reflecting a session where headline index declines remained relatively contained, but underlying participation weakened meaningfully beneath the surface.

Looking at the major indices, the pullback was broad but varied in intensity. The S&P 500 closed at 7,337.11, down 0.38%, retreating from recent highs after briefly testing a new 52-week high earlier in the session. The index opened at 7,376.78 and steadily weakened throughout the day, closing near the lower end of its intraday range.

The Dow Jones Industrial Average saw the sharpest decline, falling 0.63% to 49,596.97, once again failing to hold above the psychologically important 50,000 level. After opening above that threshold, the Dow gradually lost momentum as cyclical and industrial names came under pressure.

Meanwhile, the Nasdaq Composite proved relatively resilient, declining just 0.13% to 25,806.20 despite briefly touching fresh highs intraday. The Nasdaq continues to outperform on a relative basis, but even here momentum showed signs of slowing after a strong recent run.

This reinforces the idea that while broader indices remain near highs, leadership continues to narrow toward selective technology and growth segments, while cyclical areas are beginning to lose momentum.

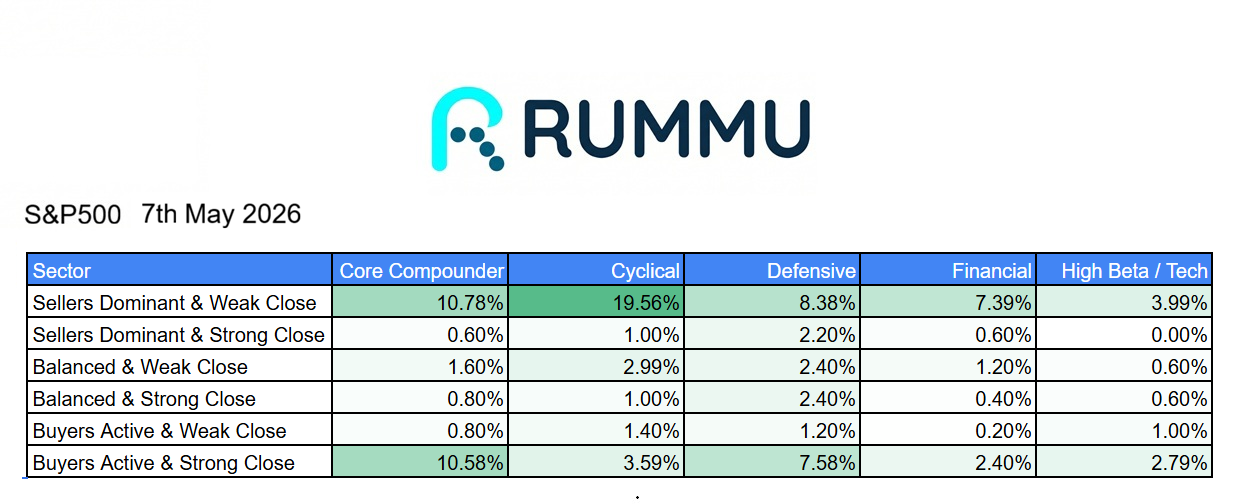

The underlying breadth data paints a more cautious picture.

Across cyclicals, 19.56% of stocks were classified as “sellers dominant with a weak close,” the highest reading across all major groups and a clear sign that economically sensitive names remained under heavy pressure throughout the session. Core compounders also saw elevated weakness, with 10.78% closing in seller-dominant territory.

At the same time, buyers remained active in selective areas. Core compounders saw 10.58% of names finish with “buyers active and strong closes,” while defensives recorded 7.58%. This suggests buyers were still present, but participation was increasingly selective rather than broad.

That shift is telling.

This was not a broad market breakdown, but it was a clear sign that participation is narrowing. Sellers had control across larger portions of the market, while buyers concentrated only in specific pockets.

Sector performance reinforces this view.

There were clear areas of strength. Specialized technology rose 4.53%, internet services gained 4.00%, ad tech climbed 3.61%, cybersecurity rose 2.89%, and data analytics added 2.79%. AI and data-related names also remained positive, rising 1.44%.

This suggests capital continues rotating toward digital infrastructure, software, and platform-driven businesses that remain tied to AI and secular technology growth themes.

However, weakness across the rest of the market was far broader.

Biotech fell 6.09%, making it the weakest segment of the session. Consumer technology declined 3.53%, brokerage fell 3.06%, industrial services dropped 2.60%, materials technology declined 2.57%, and networking fell 2.16%.

Traditional cyclical sectors also struggled, with industrials falling 2.15%, materials declining 2.14%, and banking down 1.56%.

This fragmentation continues to define the current market structure.

The indices remain near record levels, but fewer sectors are driving performance. Technology-linked infrastructure continues to absorb capital, while broader participation continues to weaken.

That dynamic can persist for longer than many expect, but it does increase fragility.

If leadership remains concentrated in AI, software, and platform names, the broader market can continue grinding higher. However, if those leadership groups begin to weaken as well, the lack of broader support could create sharper downside pressure.