Markets pulled back on Monday as rising oil prices and renewed Middle East tensions pressured sentiment, but the underlying internals were more balanced than the headline index declines initially suggest.

The S&P 500 fell 0.41% to close at 7,200.75, pulling back from recent record highs after trading in a relatively wide range between 7,174.12 and 7,244.54. The index attempted to stabilise intraday but gradually lost momentum as energy-driven inflation concerns weighed on broader risk appetite.

The Dow Jones Industrial Average saw the sharpest weakness, falling 1.13% to 48,941.90, closing near session lows after trading as high as 49,441.43 earlier in the day. That late-session weakness reflected pressure on more economically sensitive industrial names as higher oil prices raised concerns around margins and broader economic growth.

The Nasdaq was comparatively resilient, continuing the recent trend of relative outperformance as investors remained more willing to hold higher-growth technology exposure despite broader macro uncertainty.

That divergence remains one of the more consistent themes in this market.

While cyclical and industrial-heavy indices are becoming increasingly sensitive to oil volatility and geopolitical headlines, technology continues benefiting from stronger earnings momentum and structural capital flows.

The intraday breadth data helps explain why Monday’s session felt weaker in headlines than it actually was underneath.

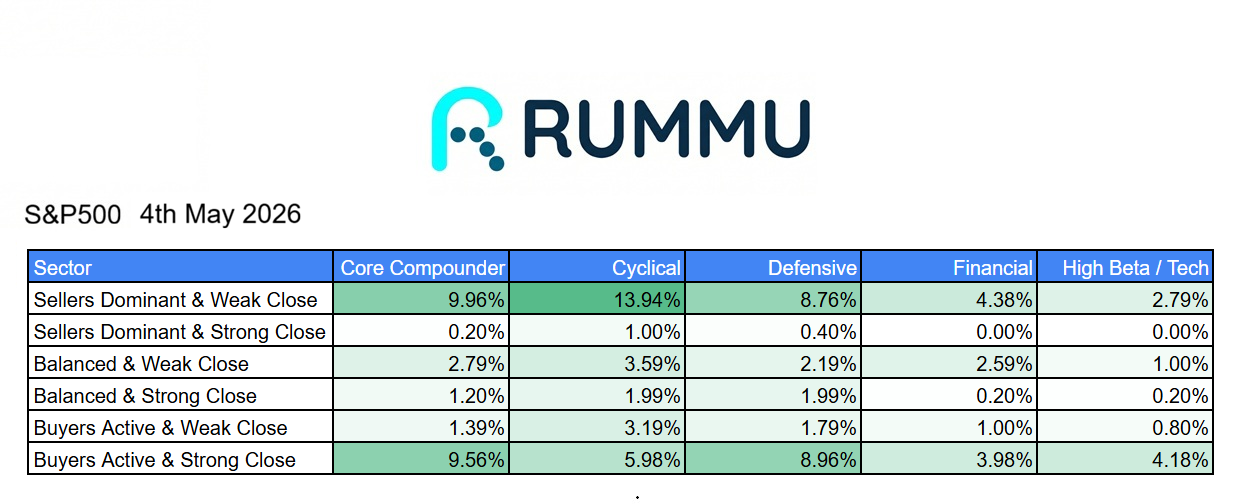

The largest concentration of weakness came from cyclicals, where 13.94% of names finished in sellers dominant with weak closes, making it the weakest group of the session. That aligns directly with the Dow’s underperformance and reflects investor caution toward economically sensitive sectors as oil prices moved higher.

Core compounders also saw notable pressure, with 9.96% finishing in sellers dominant weak close territory, while defensives came in at 8.76%.

That shows selling pressure was broad, but not overwhelmingly aggressive.

More importantly, buyers were still active beneath the surface.

Core compounders saw 9.56% of stocks finish in buyers active with strong closes, nearly offsetting the selling pressure in that category. Defensives also held up relatively well with 8.96% finishing in buyers active strong close territory.

That balance is important.

It suggests that while markets reacted negatively to macro headlines, investors were still selectively adding exposure to higher-quality names and more defensive areas rather than aggressively de-risking across the board.

Cyclicals were weaker here as well, with only 5.98% of names finishing in buyers active strong close territory, reinforcing that investors were far less willing to buy economically sensitive stocks into the close.

Financials remained relatively contained.

Only 4.38% of names finished in sellers dominant weak close territory, while 3.98% managed buyers active strong closes. That reflects a sector that weakened but avoided the sharper pressure seen across industrials and broader cyclicals.

High beta technology also remained relatively stable.

Only 2.79% of names finished in sellers dominant weak closes, while 4.18% ended in buyers active strong closes.

That continued resilience helps explain why broader market declines remained relatively contained despite the Dow’s larger selloff.

The broader takeaway is that Monday looked more like a macro-driven pause than the beginning of a broader market breakdown.

Oil-driven inflation concerns and geopolitical headlines created clear pressure, particularly in cyclical sectors, but internal market participation remained far healthier than what you would typically see during more aggressive risk-off sessions.

The S&P remains only modestly below record highs, technology continues to provide support, and buyers are still selectively stepping into quality names.

For now, this looks more like a normal consolidation following a sharp rally rather than a major shift in market structure.

The key question now is whether geopolitical tensions escalate further. If oil continues moving higher, cyclical pressure could intensify. If tensions stabilise, Monday’s weakness may prove to be a short-term reset within a still constructive broader trend.