Markets closed with a more mixed tone on Friday, and while the headline move in the S&P 500 suggested continued strength, the underlying intraday structure was notably weaker than the index finish implies.

The S&P 500 rose 0.29% to close at a fresh record high of 7,230.12, extending its rally to roughly 13% since late March and continuing to build on Thursday’s breakout above the 7,200 level. On the surface, another record close reinforces the idea that momentum remains firmly intact.

However, the intraday structure tells a more cautious story.

The index finished higher versus the previous day’s close, but notably closed well below its intraday highs after fading from the open. That type of price action often reflects early optimism being met with profit taking as the session progresses.

The Dow Jones Industrial Average declined 0.31% to 49,499.27, pulling back after briefly trading as high as 49,988.56, just shy of reclaiming the 50,000 level. The fact that the Dow closed at session lows highlights how selling pressure accelerated into the afternoon.

Meanwhile, the Nasdaq continued to lead, rising 0.89% to a fresh record close of 25,114.44, crossing the 25,000 milestone for the first time as investors continued rotating into growth and technology names.

That divergence was one of the most important developments of the session.

While the Nasdaq pushed higher, both the S&P 500 and Dow showed signs of fading momentum beneath the surface.

The intraday breadth data reinforces that caution.

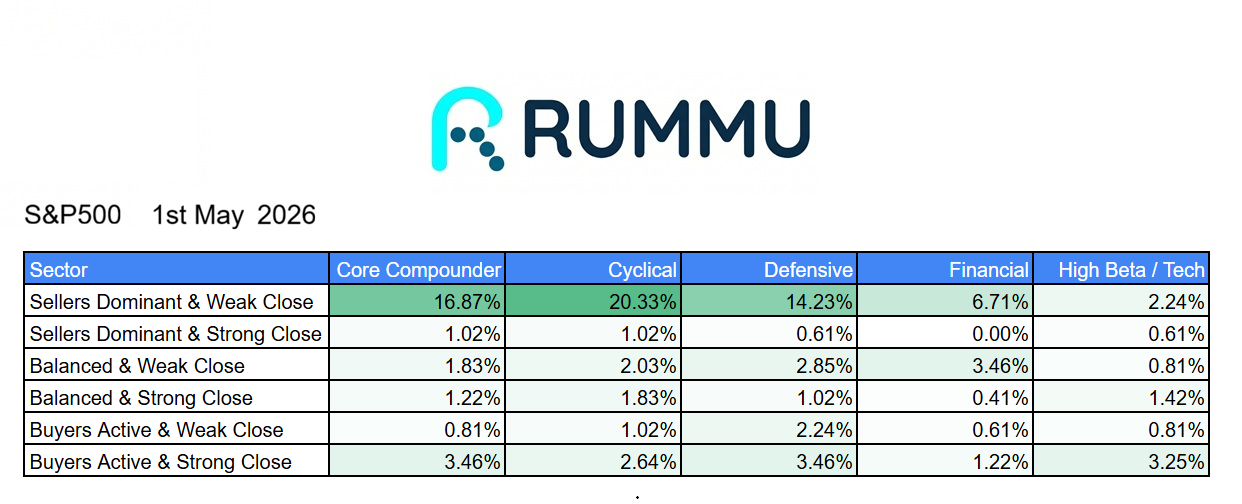

The clearest signal from Friday’s session was the dominance of sellers active with weak closes, particularly across economically sensitive sectors.

Cyclicals were the weakest group by a considerable margin, with 20.98% of names finishing in sellers dominant weak close territory. Core compounders followed at 15.89%, while defensives came in at 14.05%.

That level of broad selling pressure is difficult to ignore.

It suggests that while index performance remained resilient, a meaningful number of stocks were being sold into weakness throughout the day.

Financials were comparatively more stable, with only 6.11% of names finishing in sellers dominant weak close territory, while high beta technology remained notably resilient at just 2.04%.

That helps explain why the Nasdaq was able to outperform so significantly.

Technology leadership remained narrow but strong enough to pull the broader index higher, even as many other sectors weakened.

Buyer participation was far less convincing than Thursday’s session.

Only 3.67% of both core compounders and defensive names finished in buyers active strong close territory, while cyclicals came in at just 2.65%. Financials were particularly weak at only 1.43%, highlighting limited conviction buying into the close.

This is a meaningful shift from the prior session, where buyers controlled much of the market into the close.

Friday looked far more like selective leadership masking broader weakness.

That does not necessarily signal an immediate reversal.

Markets can remain narrow for extended periods, particularly when mega-cap technology continues attracting capital.

But it does suggest that participation is becoming less healthy as indices continue making fresh highs.

That becomes especially important after such a sharp rally.

The S&P 500 has now gained roughly 13% in just over a month, while both the S&P and Nasdaq continue printing record highs. That type of move naturally creates short-term positioning risk as investors lock in gains.

For now, momentum remains clearly positive.

Record highs across the S&P 500 and Nasdaq continue reinforcing bullish sentiment, and earnings season has largely remained supportive.

But Friday’s internal market structure was noticeably weaker than the headline index moves suggest.

If breadth continues deteriorating while indices grind higher, it would raise the probability of a short-term consolidation period.

For now, the rally remains intact.

It is simply becoming more selective beneath the surface.