Markets traded with a cautious tone yesterday, reflecting a broad but controlled sell-off beneath the surface rather than outright panic. While headline index moves appeared relatively contained, underlying breadth data painted a weaker picture, with sellers clearly dominating the session.

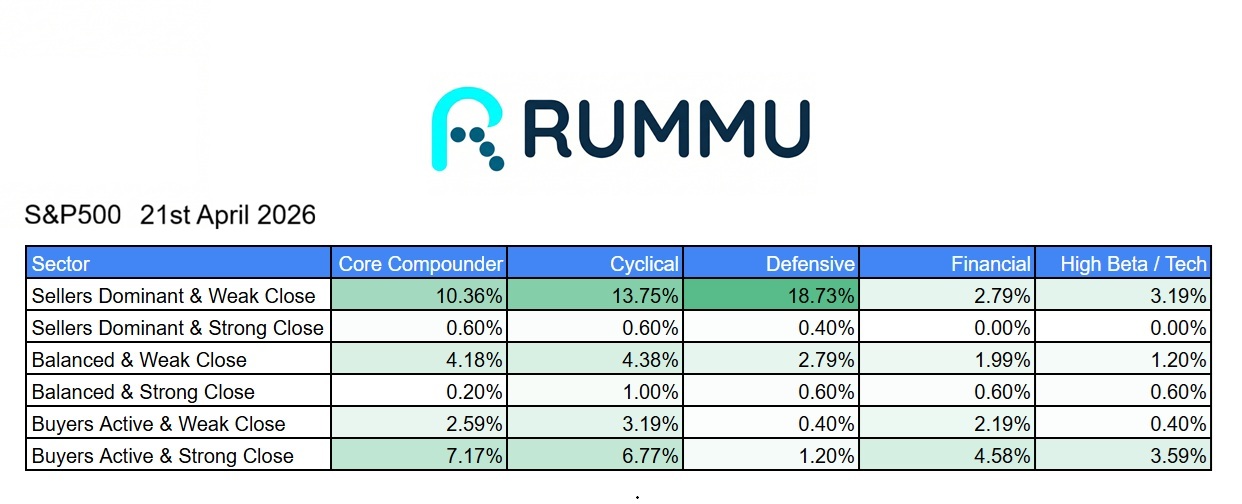

Nearly half of the S&P 500 constituents, 48.8%, were classified as “sellers dominant with a weak close,” signalling a persistent intraday downtrend that carried into the close. This is typically indicative of a distribution-type session rather than simple consolidation. In contrast, only 23.3% of stocks showed “buyers active with a strong close,” highlighting the limited strength available to offset the broader weakness.

However, the session stopped short of capitulation. The presence of both selective buying and a meaningful portion of balanced activity suggests that while sellers were in control, liquidity remained and buyers were still willing to step in at certain levels. In other words, this was pressure, not panic.

Sector dynamics reinforced this view. Defensive names, which would typically provide shelter in a risk-off environment, also experienced heavy selling pressure, while cyclicals and high-beta areas failed to offer leadership. Higher-quality compounders showed relatively better resilience, but even here the strength was selective rather than broad-based. The lack of a clear leadership group points to a market struggling for direction rather than rotating cleanly between sectors.

Importantly, this fragile and mixed market structure appears closely tied to the evolving geopolitical backdrop. Uncertainty surrounding the Iran ceasefire continues to weigh on sentiment, with markets reacting to conflicting signals around its durability. While there have been periods of optimism following extensions of the truce, the lack of a confirmed and lasting agreement has kept investors cautious. (Reuters)

This aligns with broader market behaviour observed during the conflict, where temporary relief rallies have been offset by persistent concerns around oil supply disruptions and the risk of renewed escalation. As a result, volatility remains elevated and sentiment remains highly headline-driven.

In this context, yesterday’s price action reflects a market that is neither fully risk-on nor decisively risk-off. Instead, it is operating in a state of fragile equilibrium, where sellers have the upper hand, but buyers are not fully disengaged.

Looking ahead, the key signal to watch is whether buyer participation continues to hold. A further decline in strong closes would likely confirm a transition toward a more sustained downtrend. Until then, the market remains vulnerable to continued chop, with macro developments, particularly around the Iran ceasefire, acting as the primary catalyst for direction.

The big winner of the day on the S&P 500 were HP Inc. (HPQ) with a close up 7.16% from open price. This was followed by Northern Trust (NTRS) with a close up 6.04% from open price.

- S&P 500 closing price 7,064.01 (-0.63%)

- Dow Jones closing price 49,149.38 (-0.59%)

- Nasdaq Composite closing price 24,259.97 (-0.59%)