U.S. equities began June on a positive note, with the S&P 500 and Nasdaq once again reaching fresh record territory as investors continued to embrace technology, software and AI-related opportunities. While the headline gains were relatively modest, underlying market leadership remained concentrated in growth-oriented sectors that have driven much of 2026’s advance.

The S&P 500 rose 19.90 points, or 0.26%, to close at a new all-time high of 7,599.96. The index traded within a range of 7,562.61 to 7,617.66 during the session, demonstrating resilience despite some pockets of profit-taking across defensive areas of the market.

The Nasdaq Composite outperformed once again, advancing 0.42% to 27,086.81 as technology stocks extended their recent momentum. The rally was driven by continued enthusiasm surrounding artificial intelligence infrastructure spending and strong performance from several mega-cap technology leaders.

NVIDIA remained at the centre of market attention, surging more than 6% as investors continued to reward companies directly benefiting from accelerating AI adoption. Microsoft also posted strong gains, adding between 2% and 5% depending on the session measure, further supporting the broader technology complex. Intel moved in the opposite direction, falling roughly 4.7% as investors continued to favour companies with stronger AI positioning and earnings momentum.

The Dow Jones Industrial Average lagged the technology-heavy indices, gaining just 46 points, or 0.09%, to trade around 51,078. The divergence between the Dow and Nasdaq highlighted the continued concentration of market leadership within growth-oriented sectors rather than broad-based participation across traditional blue-chip stocks.

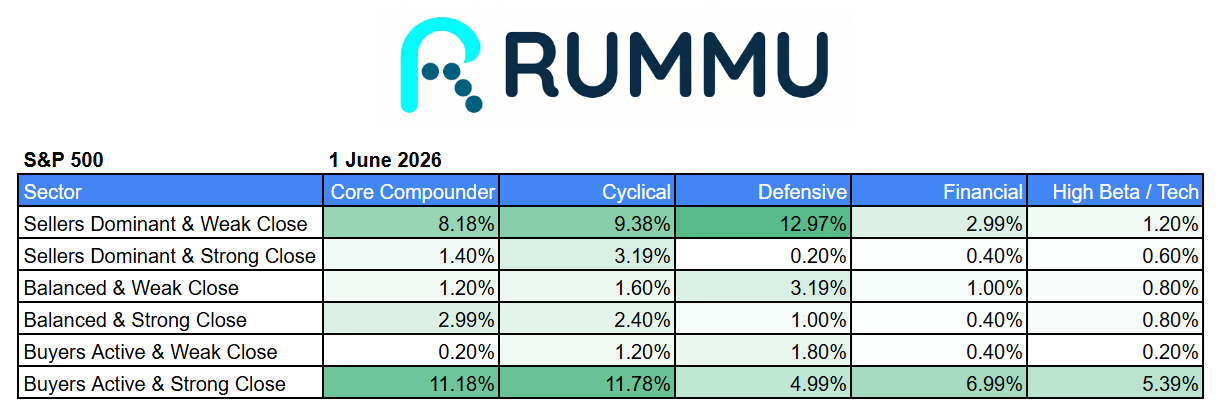

RUMMU intraday market data showed a more nuanced picture beneath the surface. Core Compounders and Cyclicals both recorded strong buying activity, with more than 11% of constituents in each group finishing the day in the “Buyers Active & Strong Close” category. This suggests investors remained willing to deploy capital into quality growth businesses and economically sensitive sectors despite the market sitting at record highs.

However, defensive sectors displayed a different character. Nearly 13% of defensive stocks finished in the “Sellers Dominant & Weak Close” category, the highest reading among the major groups. This indicates investors continued rotating away from traditionally defensive areas and toward growth opportunities, reinforcing the risk-on tone that has characterised recent market action.

The sector heatmap revealed where buyers were concentrating their attention. Cloud & SaaS led the market with a gain of 10.21%, while Internet Services rose 8.82%. Cybersecurity advanced 5.30%, Hardware gained 5.28%, and IT Services climbed 5.03%. Specialized Technology, Payroll, Data & Analytics and Internet Infrastructure also posted strong gains.

The leadership profile continues to reflect the market’s focus on digital transformation and AI-related investment themes. Software gained 3.25%, Advertising rose 3.29%, Networking advanced 2.89%, and Financial Infrastructure added 2.19%, highlighting the broad participation across technology-adjacent industries.

Not all areas shared in the optimism. Biotech declined 2.15%, Energy Infrastructure fell 2.60%, Automotive Technology lost 2.72%, and Exchange-related businesses dropped 2.33%. Defensive consumer sectors also struggled, with Consumer Defensive stocks falling 0.95% and Staples slipping 0.60%.

Perhaps most notable was the continued strength in Cloud & SaaS. The sector has experienced significant volatility over the past several years, but Monday’s strong performance suggests investors remain willing to reward software businesses capable of delivering durable growth in an environment increasingly shaped by AI adoption and enterprise digital spending.

The session reinforced a familiar theme for 2026. While major indices continue to reach new highs, the underlying drivers remain concentrated in technology, software and AI-linked businesses. Beneath the surface, investors are showing increasing willingness to rotate out of defensive sectors and into higher-growth opportunities, suggesting confidence remains elevated despite record valuations across parts of the market.

For now, the path of least resistance remains higher, particularly for companies benefiting from artificial intelligence, cloud infrastructure and digital transformation trends. The question for investors is whether this leadership can continue broadening beyond technology or whether market performance will remain concentrated among a relatively small group of growth-oriented winners.