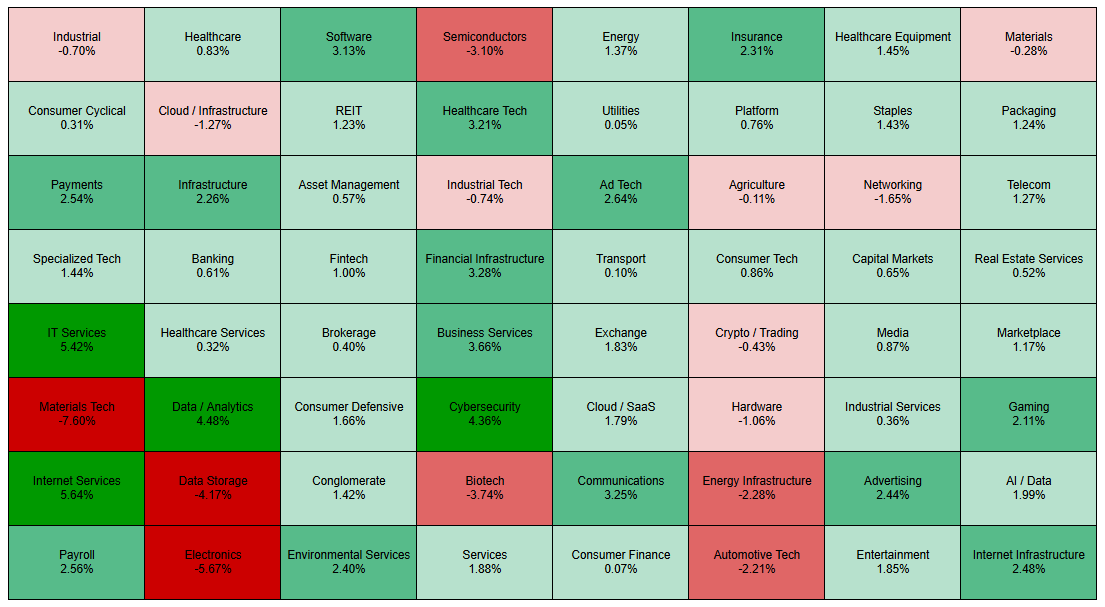

Last week’s S&P 500 action painted a picture of a market that remained constructive at the index level, but with increasingly selective leadership beneath the surface. While the broader benchmark continued to hold near record highs, intraday behaviour suggested investors were rotating aggressively between sectors rather than simply buying the market indiscriminately.

Technology remained one of the most influential forces, but leadership became far more fragmented. Software rose 3.1% during the week, while ad tech gained 2.6%, cybersecurity climbed 4.4%, and data and analytics advanced 4.5%, showing that investors continued to reward selective digital infrastructure and software businesses tied to productivity and AI-related spending. Internet services also surged 5.6%, reinforcing appetite for selective growth names. However, that strength was offset by notable weakness in semiconductors, which fell 3.1%, data storage dropped 4.2%, and electronics slumped 5.7%. Materials technology was one of the week’s sharpest laggards, down 7.6%, highlighting profit taking in areas that had previously led the rally.

What makes this particularly interesting is that software has not been a leadership group in 2026. In fact, software remains down more than 26% year to date, while semiconductors, networking, cloud infrastructure and hardware have been some of the market’s strongest performers, with gains ranging from roughly 45% to nearly 190% in some areas. Data storage is up almost 190% year to date, materials technology has surged more than 118%, electronics are up over 92%, while semiconductors and networking have both gained more than 66%. This tells the broader story of this year’s technology trade. Investors have aggressively rewarded the infrastructure layer of AI, including chips, hardware, networking and data centre buildout, while much of the software and application layer has lagged badly.

That makes last week’s move more notable. Software gained 3.1%, cybersecurity rose 4.4%, data and analytics climbed 4.5%, and internet services surged 5.6%, even as semiconductors and hardware-linked groups saw weakness. Rather than simply showing broad technology strength, this may reflect a rotation into underowned laggards after a prolonged infrastructure-led rally.

That kind of rotation can be an important signal. It often reflects a shift from chasing the most explosive AI infrastructure stories toward businesses with more recurring revenue, margin durability and cash flow characteristics. Investors may still want technology exposure, but are becoming more selective about where they are willing to pay premium valuations.

Financials showed a steadier tone. Financial infrastructure gained 3.3%, exchanges rose 1.8%, payments advanced 2.5%, and broader banking and capital markets remained positive, though without aggressive momentum. This points to a market still comfortable with economically sensitive areas, but not yet seeing financials as the primary leadership engine.

Healthcare was another area of quiet strength. Healthcare technology gained 3.2%, healthcare equipment rose 1.5%, and insurance climbed 2.3%, showing investors were still adding exposure to defensive growth sectors even as some higher beta areas cooled. Traditional healthcare services were more muted, but the overall tone was constructive.

Industrials and infrastructure delivered a mixed but important signal. Infrastructure gained 2.3%, business services rose 3.7%, communications advanced 3.3%, and environmental services gained 2.4%, suggesting investors still see strength in real economy spending and infrastructure-related demand. However, broader industrials slipped modestly, while industrial tech and industrial services were softer, showing selective rather than broad-based participation.

Consumer-related sectors also reflected a split tone. Consumer defensives gained 1.7%, staples rose 1.4%, and entertainment climbed 1.9%, while consumer cyclical and consumer tech posted modest gains. That points to a market still willing to own consumption-related businesses, but with a preference for quality and resilience rather than aggressive discretionary risk.

Perhaps the most interesting signal came from defensives and quality sectors quietly outperforming alongside pockets of growth. Insurance, staples, healthcare, consumer defensive and utilities all held up, suggesting that investors were still maintaining some protection beneath the surface even as the S&P 500 remained close to record highs.

The overall takeaway from last week is that the index may have looked stable, but leadership became much more selective underneath. Money was still flowing into software, cybersecurity, internet services, financial infrastructure and defensive quality names, while semiconductors, hardware and materials-linked technology saw notable selling pressure. This looks less like a broad risk-on melt-up and more like a market beginning to rotate internally, favouring quality growth and selective defensives while trimming exposure in areas that had become overheated. If software can continue building on this strength after struggling for much of the year, it may signal that market leadership is starting to broaden beyond the AI hardware trade and into the next layer of technology beneficiaries.