U.S. markets closed higher on Friday, with the S&P 500 continuing its push toward fresh highs as investors balanced optimism around earnings and improving geopolitical sentiment against a more selective tone beneath the surface. The index gained 27.75 points, or 0.37%, to finish at 7,473.47, trading in a relatively tight range before closing near the upper end of the session and remaining just below its recent record high.

The Dow Jones Industrial Average led the major benchmarks, rising 294 points, or 0.58%, to close at a fresh record of 50,579.70. Blue-chip names found support from strong corporate earnings, with Merck leading gains after jumping more than 5%, while Salesforce and Cisco also added to the advance. The Nasdaq Composite lagged but still closed modestly higher, gaining 0.19% as technology leadership cooled, held back in part by weakness in Nvidia, Walmart, and Amazon.

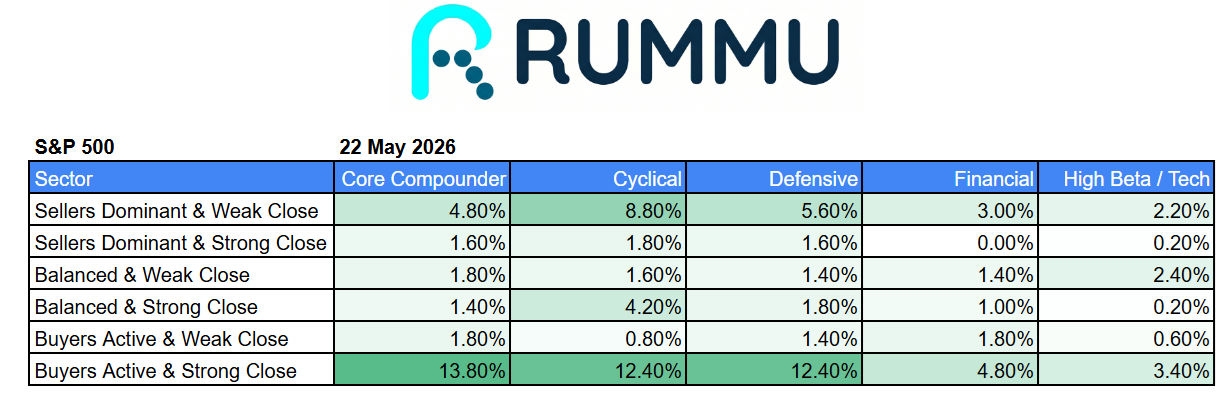

Looking beneath the headline numbers, the intraday sector picture suggested a market that was constructive but selective rather than aggressively risk-on. Core compounders showed the strongest breadth, with 13.8% of the group closing in the buyers active and strong close category, reinforcing steady institutional demand in quality names. Defensives matched that strength at 12.4%, showing that investors were still willing to hold protection even as the broader market advanced.

Cyclicals also posted healthy participation, with 12.4% of names closing in buyers active and strong close territory, but there was still notable weakness under the surface, with 8.8% of cyclical stocks remaining in sellers dominant and weak close conditions. That suggests the rally was not a broad all-clear move, but one where money was flowing selectively into stronger setups while weaker economically sensitive names still struggled.

Financials were more muted, with only 4.8% in buyers active and strong close positioning, pointing to a more cautious tone despite the broader market’s gains. High beta and technology names also lacked broad leadership, with just 3.4% showing strong buying closes, reinforcing the idea that while indexes moved higher, the market’s speculative edge remained restrained.

The overall takeaway from Friday’s session was a market that continued grinding higher, supported by quality leadership and resilient breadth in core compounders and defensives, but without the broad speculative surge often seen in full risk-on rallies. The S&P 500 remains close to record highs, but beneath the surface, investors still appear selective, favouring quality and stability over aggressive momentum chasing.