The market pushed to fresh highs on Thursday, but beneath the headline strength the session was far more selective than the index numbers suggested.

The S&P 500 closed at a record 7,501.24, rising 56.99 points or 0.77% after trading between 7,454 and 7,517. The Dow Jones Industrial Average added 370 points, or 0.75%, to finish above the psychologically important 50,000 level at 50,063. Meanwhile the NASDAQ Composite climbed 0.88% to 26,635 as investors continued rotating back into growth names.

At first glance it looked like a broad risk-on rally. The reality was more nuanced.

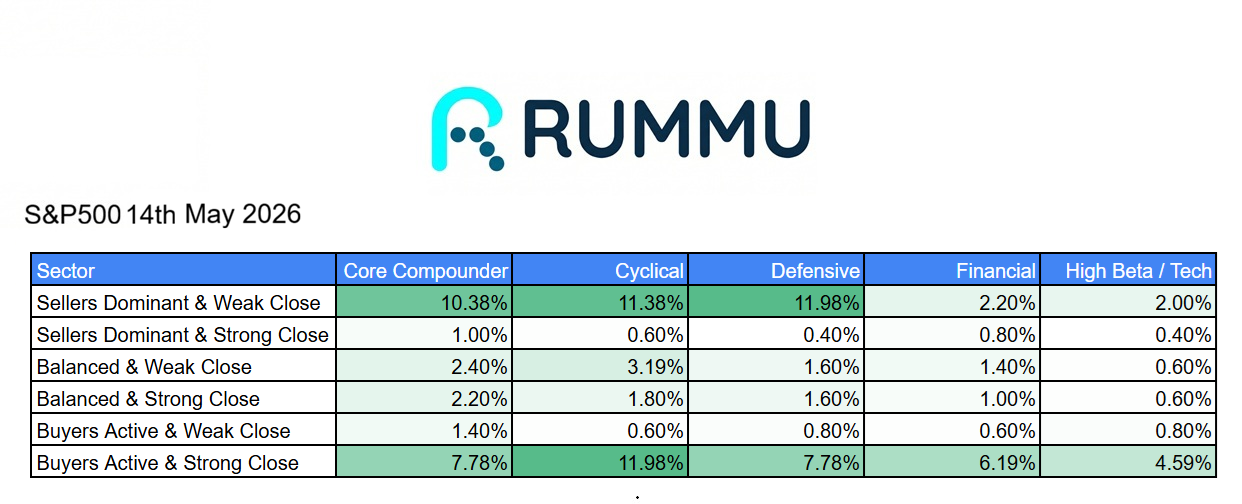

Rummu sector positioning data shows sellers were still highly active across large parts of the market. Defensive stocks saw 11.98% of names finish in “Sellers Dominant and Weak Close,” while cyclicals came in at 11.38% and core compounders at 10.38%. That tells you plenty of stocks spent most of the session under pressure despite the indices finishing strongly.

The difference came late in the day, where buyers stepped in aggressively. Cyclicals led with 11.98% of names finishing in “Buyers Active and Strong Close,” followed by core compounders and defensives at 7.78%. Financials also quietly improved, with 6.19% of stocks finishing with strong buying pressure into the close.

That late-session buying explains why the indices looked cleaner than the underlying breadth initially suggested. The market spent part of the day digesting gains before institutions stepped back into risk.

Technology once again carried much of the momentum.

AI and data infrastructure stocks remained a clear leadership pocket, gaining 3.15%, while specialized tech rose 2.90%, fintech climbed 2.41%, cybersecurity added 2.69%, and software advanced 1.32%. Networking stocks also gained 1.39%, likely helped by strong earnings momentum from Cisco after its AI infrastructure commentary reinforced confidence in broader enterprise networking demand.

Crypto-linked names were among the biggest winners of the day, surging 5.35%, while ad tech rose 3.53% and entertainment stocks gained 2.94%, showing investors were comfortable moving further out on the risk curve.

The rally wasn’t broad enough to ignore weakness.

Real estate services fell sharply by 6%, financial infrastructure dropped 2.69%, packaging declined 2.18%, healthcare services fell 2.44%, and traditional infrastructure names dropped 2.14%. Advertising stocks also struggled, down nearly 4%.

This increasingly looks like a market rewarding future growth narratives while punishing anything tied to slowing economic sensitivity or weaker near-term fundamentals.

That matters because the S&P 500 continues climbing despite narrowing leadership. When record highs are being driven primarily by AI infrastructure, software, semiconductors and select growth industries, investors should pay close attention to whether participation broadens or narrows further.

For now, the bulls remain firmly in control. The S&P pushed to another all-time high, the Dow reclaimed 50,000, and buyers once again showed up when it mattered most.

But under the surface, this still feels like a market where stock selection matters far more than simply buying the index.