U.S. markets ended the week on a weaker note Friday as rising oil prices and surging Treasury yields sparked a broad selloff, with growth stocks absorbing the heaviest pressure after an extended rally.

The S&P 500 fell 1.24% to 7,408.50, closing down 92.74 points, while the Nasdaq Composite dropped 1.54% to 26,225.14, shedding 410 points as investors rotated out of higher-multiple technology names. The Dow Jones Industrial Average declined 537 points (-1.07%) to 49,526.17.

Despite the sharp daily decline, the S&P 500 still secured its seventh consecutive weekly gain, highlighting just how strong the broader market trend has been in recent months.

The intraday chart shows the S&P 500 attempted to stabilize early in the session before selling pressure accelerated into the afternoon, with buyers largely absent into the close.

The biggest catalyst was a sharp move in energy markets. Brent crude surged above $109 per barrel, reigniting inflation concerns at a time when investors had become increasingly comfortable with the idea of easing price pressures. Higher oil prices raise concerns that inflation could remain sticky for longer — something the bond market reacted to quickly.

That reaction was most visible in Treasuries, where the 30-year yield climbed to 5.127% — its highest closing level since 2007. Rising long-term yields tend to pressure equities by increasing borrowing costs and reducing the present value of future earnings, particularly for high-growth technology companies.

That pressure was felt across semiconductors, where recent winners saw notable profit taking. NVIDIA, Advanced Micro Devices and Intel all moved lower as investors locked in gains following a strong run in AI-related names.

Looking at a sector heatmap reflected that broader weakness beneath the surface.

Crypto/Trading stocks led declines, falling 4.96%, while Packaging (-3.70%), Telecom (-3.44%), Materials Tech (-3.18%), and Automotive Tech (-2.71%) were also among the market’s weakest areas.

Interestingly, there were still pockets of strength:

- Ad Tech: +3.87%

- Cloud/SaaS: +3.74%

- Data Storage: +2.28%

- Cybersecurity: +2.02%

- Software: +1.79%

That suggests this wasn’t indiscriminate panic selling. Investors were selective, rotating away from rate-sensitive areas while continuing to reward businesses with strong structural growth narratives.

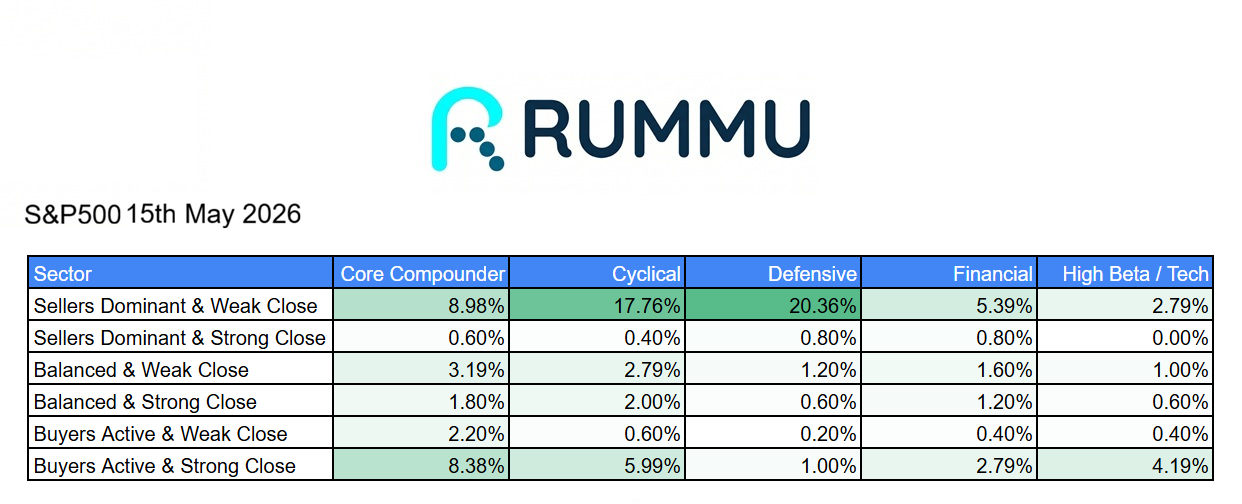

Rummu market breadth table tells a similar story.

Defensive sectors saw the heaviest selling pressure, with 20.36% of defensive stocks closing as “seller dominant & weak close,” suggesting broad institutional distribution. Cyclicals also showed weakness, with 17.76% finishing in that same category.

Meanwhile, Core Compounders remained far more resilient, with 8.38% closing as “buyers active & strong close,” nearly matching the percentage of weak closes. That’s often a sign that high-quality businesses continue attracting capital even during broader market pullbacks.

That may be the most important takeaway from Friday’s session.

Yes, yields are rising. Yes, oil is creating fresh inflation concerns. And yes, momentum stocks finally paused.

But underneath the headline decline, investors still appear willing to buy durable businesses on weakness. A sign this may be more of a healthy reset than the start of a broader risk-off move.

After seven straight weekly gains, the market may simply be reminding investors that even strong bull markets rarely move in a straight line.