At the index level, the technology sector continues to project strength, supported by ongoing enthusiasm around artificial intelligence and infrastructure buildout. However, beneath the surface, performance has become increasingly fragmented, revealing a clear divergence between hardware-linked businesses and software-driven models.

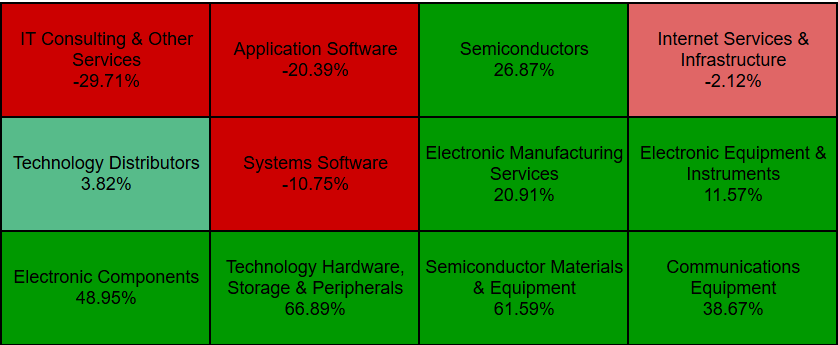

Year-to-date returns (22nd April 2026) across the Information Technology sector highlight this split.

On one side, hardware, semiconductors, and infrastructure-related segments are delivering exceptional performance. Technology hardware, storage and peripherals are up 66.89%, semiconductor materials and equipment have gained 61.59%, and electronic components are higher by 48.95%. Communications equipment and electronic manufacturing services have also posted strong gains, up 38.67% and 20.91% respectively, while semiconductors themselves have risen 26.87%.

This cluster is not random. It reflects a concentrated wave of capital flowing into the physical layer of the AI ecosystem. As demand for compute, storage, and connectivity accelerates, companies tied directly to the buildout of infrastructure are seeing both revenue growth and multiple expansion. The beneficiaries are those supplying the tools, components, and systems required to support this cycle.

The leadership group reinforces this narrative. Names such as Western Digital (WDC), Seagate Technology (STX), Teradyne (TER), and Corning (GLW) have all delivered outsized gains, supported by improving demand visibility and positioning within the broader infrastructure theme. While SanDisk (SNDK) appears as a top performer, its recent listing in April means its contribution should be viewed in context rather than as a reflection of sustained outperformance.

- Sandisk +300%

- Western Digital +120%

- Ciena +107%

- Seagate Technology +106%

- Teradyne +93%

- Coming Inc. +90%

In contrast, software and services are telling a very different story.

Application software is down 20.39% year-to-date, systems software has declined 10.75%, and IT consulting and services have fallen sharply by 29.71%. Internet services and infrastructure have also remained under pressure, down 2.12%. More importantly, the weakest individual performers are concentrated in this segment, with EPAM Systems (EPAM), Gartner (IT) , Intuit (INTU) , Workday (WDAY), and Fair Isaac (FICO) all posting declines between 37% and 43%.

This divergence is not simply a rotation. It reflects a reassessment of growth durability and valuation during a period of AI expansion. The market is questioning whether software companies can retain value against the new Tech of artificial intelligence.

Software businesses, particularly those with subscription-based models, were previously valued on the assumption of consistent, high-margin growth. However, as enterprise spending becomes more selective and budgets shift toward infrastructure and AI deployment, demand visibility for traditional software solutions has weakened. At the same time, elevated starting valuations have left little room for disappointment, resulting in multiple compression across the group.

In effect, capital is being reallocated away from perceived “asset-light” growth and toward companies with direct exposure to the AI buildout. The market is favouring tangible demand, visible order books, and near-term revenue realisation over longer-duration growth narratives.

Technology is not moving as a single entity. It is splitting into two distinct groups: those enabling the infrastructure behind the next wave of compute, and those reliant on enterprise spending cycles that are becoming increasingly constrained.

This has important implications.

First, index-level strength may overstate the health of the sector. Gains are being driven by a relatively narrow set of industries, masking weakness elsewhere. Second, the traditional assumption that software provides defensive growth within technology is being challenged, as these businesses prove more sensitive to macro and spending shifts than previously assumed.

Finally, this divergence suggests that the current cycle is not just about technology adoption, but about where that adoption is occurring. The market is prioritising the build phase over the utilisation phase. For now, in technology, the builders are winning.