Markets returned to risk-on mode Tuesday, with major indices pushing back to record highs, but the underlying session was more selective than the headline moves initially suggest.

The S&P 500 closed at a new all-time high of 7,259.22, up 0.81%, after trading in a relatively controlled intraday range between 7,233.62 and 7,273.26. The Nasdaq Composite also reached fresh record highs, gaining 1.03% to close at 25,326.13, while the Dow Jones Industrial Average added 0.73% to finish at 49,298.25.

At the index level, it looked like a broad continuation rally following Monday’s geopolitical-driven weakness as oil prices pulled back and investors rotated back into growth.

Underneath the surface, however, participation remained far more uneven.

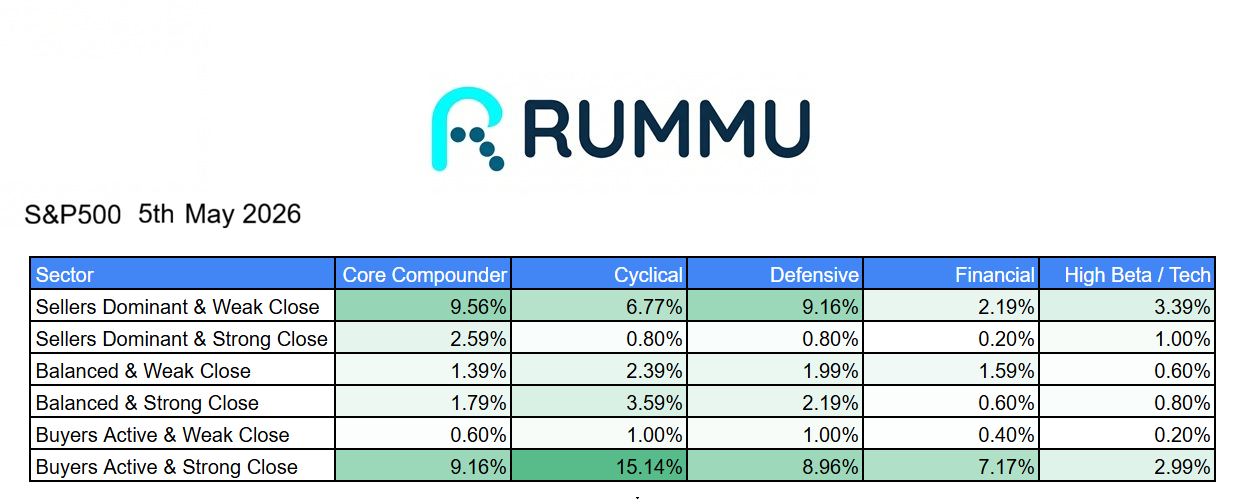

The intraday breadth data shows that 39.02% of stocks finished in “buyers active with a strong close” territory, compared with 28.68% that closed in “sellers dominant with a weak close.”

That represents a constructive shift from Monday’s defensive tone, but it was not an overwhelming broad-market buying surge.

The strongest participation came from cyclicals, where 15.14% of names closed with buyers firmly in control, which suggests investors were willing to rotate back into economically sensitive areas after Monday’s risk-off move.

Core compounders also showed healthy participation at 9.16%, while defensives came in at 8.96%, reflecting a market that was broadening modestly beyond just mega-cap technology.

Financials were constructive as well, with 7.17% of names closing in buyers active with a strong close territory, helping support the Dow’s rebound.

Where things become more interesting is at the industry level.

The biggest leadership came from areas directly tied to AI infrastructure and growth spending.

Cloud infrastructure surged 8.50%, one of the strongest groups in the market and a major driver behind Nasdaq leadership. That move was reinforced by continued strength in semiconductors, which gained 2.60%, as investors reacted positively to ongoing AI-related earnings momentum.

That strength aligns directly with the market’s reaction to recent semiconductor earnings, where investors continue rewarding companies tied to AI compute buildouts.

Healthcare services also posted a notable 8.27% gain, while data storage rose 3.38%, agriculture gained 2.69%, and advertising added 1.98%.

These moves suggest investors were not simply crowding into one narrow theme, but selectively rotating into areas showing strong earnings momentum and improving operational trends.

At the same time, weakness remained concentrated in more speculative areas.

Crypto and trading stocks fell 5.33%, making them one of the weakest areas of the session. Specialised technology declined 3.92%, while AI and data names fell 3.12% despite broader semiconductor strength.

That divergence is important.

It suggests investors are becoming increasingly selective within growth. They are rewarding companies tied to actual infrastructure deployment and earnings visibility, while pulling capital away from higher-multiple speculative names.

Biotech also remained weak, falling 2.03%, while healthcare technology dropped 1.73% and consumer technology declined 1.65%.

This reinforces that the rally remains highly selective rather than universally bullish.

The intraday structure also supports that view.

Despite finishing near session highs, a meaningful portion of the market still spent the day under selling pressure. 21.91% of stocks finished in “sellers dominant with weak closes,” while another portion remained balanced or failed to hold stronger intraday momentum.

That tells us this was not a session where buyers completely overwhelmed sellers.

Instead, leadership remained concentrated in areas with the strongest earnings revisions, particularly semiconductors, cloud infrastructure, and enterprise AI exposure.

That continues to define this market.

The S&P 500 and Nasdaq are making new highs, but leadership remains highly concentrated around earnings-driven technology names and selective cyclical recovery trades.

The good news is that breadth improved versus Monday and buyers regained control in key sectors.

The risk is that participation still remains uneven, and areas outside the current leadership group continue to struggle attracting sustained capital.

For now, the broader trend remains constructive.

New highs across the S&P 500 and Nasdaq, improving cyclical participation, and continued semiconductor leadership all point toward a market that remains willing to buy dips.

But the session also reinforced an increasingly familiar pattern, the market is moving higher, just not evenly.