Markets finished April with a strong risk-on tone on Thursday, but what stood out beneath the headline gains was how broad participation remained throughout the session…even if some areas of the market showed less conviction into the close.

The S&P 500 rose 1.02% to close at a fresh record high of 7,209.01, marking its first-ever close above the 7,200 level. The index traded within a relatively controlled intraday range of 7,126.15 to 7,219.83, steadily building momentum throughout the day before closing near session highs. The move capped off an exceptional month for equities, with the S&P 500 gaining 10.4% in April, its strongest monthly performance since 2020.

The Nasdaq Composite also reached a record close, rising 0.89% to 24,892.31, continuing the leadership seen across growth and technology names. Meanwhile, the Dow Jones Industrial Average outperformed, climbing 1.62% to 49,652.14, adding nearly 800 points as broader cyclical and industrial exposure participated in the rally.

While the index performance was impressive on its own, the real story came from the underlying intraday participation data.

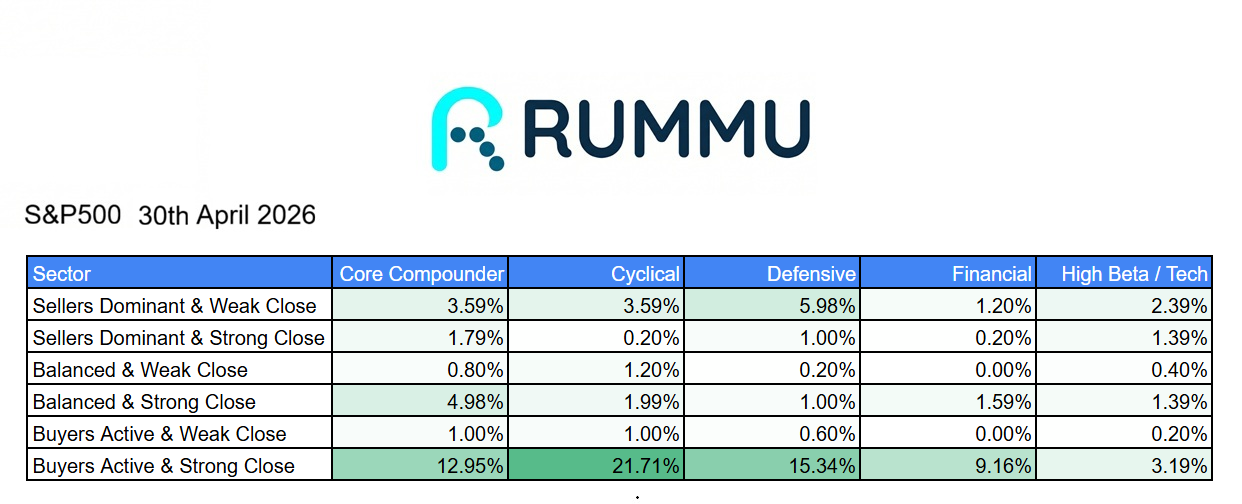

The strongest signal from the session was the dominance of buyers active with strong closes, which typically reflects institutional conviction rather than short-term intraday chasing.

Cyclical stocks led this category by a wide margin, with 21.71% of names finishing in this strongest possible intraday structure. Defensive stocks followed at 15.34%, while Core Compounders posted 12.95% and Financials came in at 9.16%.

That combination is particularly notable.

When cyclicals lead aggressive buying activity, it usually reflects growing confidence in economic sensitivity and earnings durability. But seeing defensives also participate strongly suggests this wasn’t purely speculative risk-taking — investors were broadly allocating across multiple areas of the market rather than crowding into a narrow theme.

Core compounders also continued to attract meaningful flows, reinforcing that high-quality secular growth remains firmly supported even at elevated valuations.

The weaker side of the data tells a more balanced story.

Defensives saw 5.98% of stocks finish in “sellers dominant, weak close”, the highest among all sectors in that category. Core compounders and cyclicals both registered 3.59%, while high beta technology saw 2.39%.

This suggests some profit-taking remained present beneath the surface, particularly in areas that have recently outperformed.

However, what’s important is that this selling pressure largely failed to overwhelm broader buying activity.

Even in high beta technology — often the area most vulnerable to sharp reversals after strong monthly runs — only 3.19% of names finished in buyers active strong close territory. That may indicate some rotation away from pure speculative growth and toward broader market participation.

That dynamic helps explain why the Dow materially outperformed both the Nasdaq and S&P 500.

Rather than another narrow mega-cap technology driven rally, Thursday’s session looked far healthier from a market structure perspective.

Investors were buying industrials, financials, defensives, and quality compounders simultaneously — a much broader and more sustainable form of strength.

The broader takeaway is that markets are entering May with strong momentum, improving breadth, and renewed investor confidence following a volatile first quarter.

After concerns surrounding rates, geopolitics, and earnings volatility earlier in the year, markets appear increasingly comfortable focusing on resilient economic data, strong corporate earnings, and continued AI-driven investment trends.

The primary near-term risk now may simply be positioning.

After the S&P 500’s strongest monthly gain since 2020 and multiple indices sitting at record highs, expectations are becoming increasingly elevated.

But Thursday’s session suggested this rally remains supported by far healthier internal participation than many would expect at new highs, this remains an encouraging signal heading into May.