US equities finished the session modestly higher, though the headline gains masked a clear divergence beneath the surface. The S&P 500 advanced 16.43 points (+0.22%) to close at 7,580.06, while the Nasdaq Composite gained 55.15 points (+0.20%) to 26,972.62. The standout performer was the Dow Jones Industrial Average, which rose 363.49 points (+0.72%) to close at a new all-time high of 51,032.46.

The broader market spent much of the session consolidating after recent gains. The S&P 500 traded between 7,563.55 and 7,599.38 before finishing near the middle of its daily range. The Nasdaq also struggled to build momentum despite strength in several large technology names, suggesting investors remained selective rather than broadly risk-seeking.

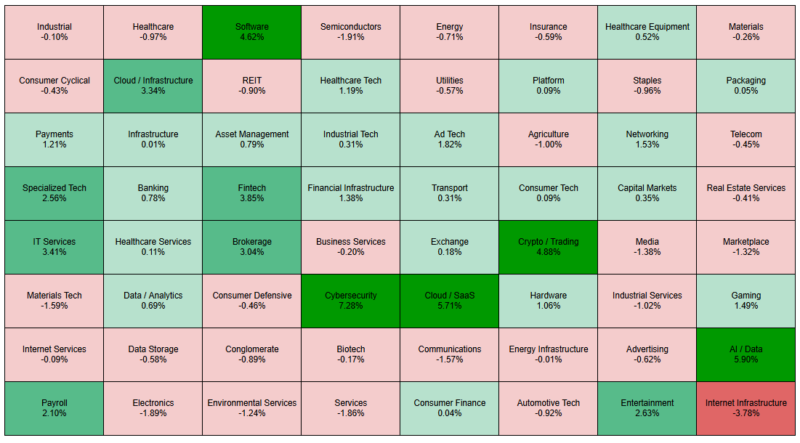

The day’s leadership came from software and enterprise technology. IBM surged 12.90%, Salesforce gained 8.46%, and Microsoft advanced 5.45%, helping support both the Dow and technology sectors. This strength was reflected in sector performance, where Software (+4.62%), Cloud/SaaS (+5.71%), Cybersecurity (+7.28%), AI/Data (+5.90%), Fintech (+3.85%), IT Services (+3.41%), and Cloud Infrastructure (+3.34%) all posted strong gains. The market continues to reward companies viewed as beneficiaries of AI adoption, enterprise software spending, and digital infrastructure investment.

At the other end of the market, defensive and traditional sectors lagged. Walmart fell 2.61%, Johnson & Johnson declined 2.41%, and Nike dropped 2.41%. Utilities (-0.57%), Consumer Defensive (-0.46%), Staples (-0.96%), Insurance (-0.59%), Energy (-0.71%), and Healthcare (-0.97%) all underperformed. This rotation away from defensive sectors and into growth-oriented technology suggests investors were willing to increase risk exposure despite markets trading near record highs.

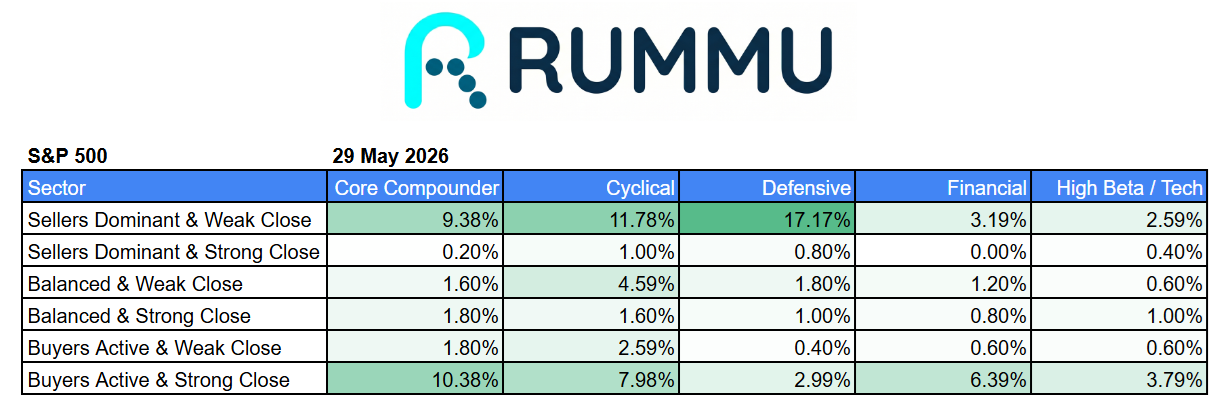

Market breadth presented a more balanced picture than the technology-led rally might suggest. Within the S&P 500, Core Compounders showed the strongest behaviour profile, with 52 stocks closing in the “Buyers Active & Strong Close” category compared to 47 in “Sellers Dominant & Weak Close.” Financials also displayed notable strength, with 32 stocks closing under active buying pressure versus only 16 exhibiting weak closes. High Beta and Technology stocks remained constructive, although participation was less broad than in previous sessions.

Defensive sectors were noticeably weaker. A total of 86 defensive stocks closed in the “Sellers Dominant & Weak Close” category, representing over 17% of the index. This suggests that while headline indices finished higher, institutional capital continued rotating away from traditionally defensive areas and toward growth, software, and AI-linked opportunities.

The intraday heatmap reinforced this theme. Cybersecurity, AI/Data, Cloud/SaaS, Crypto & Trading, Software, Fintech, Brokerage, and IT Services all recorded some of the strongest gains of the day. Meanwhile, Internet Infrastructure, Semiconductors, Electronics, Communications, Media, and Energy-related sectors lagged, indicating investors were favouring software monetisation and AI applications rather than hardware and infrastructure providers.

Overall, the session can best be characterised as a selective risk-on day. Technology leadership remained intact, software and AI-related businesses attracted significant buying interest, and financials continued to participate in the advance. However, the relatively modest gains in the S&P 500 and Nasdaq, combined with weakness in defensive sectors, suggest the market remains highly concentrated around specific growth themes rather than experiencing a broad-based rally.