US markets pushed higher yesterday, with the S&P 500 gaining 1.05% to close at 7,137.90, the Nasdaq rising 1.64% to 24,657.57, and the Dow Jones adding 0.69% to 49,490.03. Despite the positive headline performance, underlying breadth data suggests a more mixed and fragile structure beneath the surface.

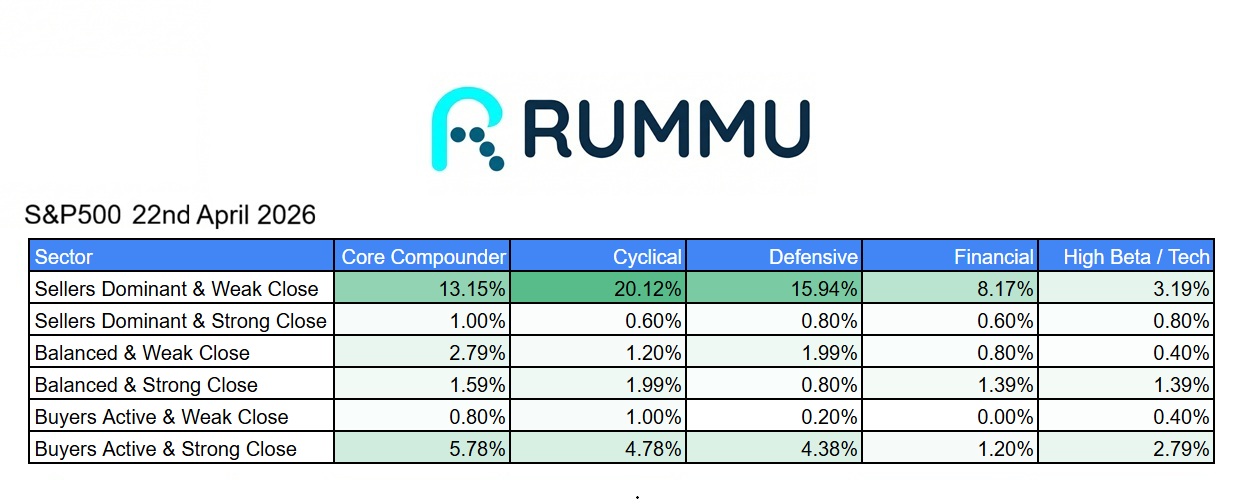

A significant portion of the market remained under pressure, with 20.12% of cyclical stocks and 15.94% of defensive names classified as “sellers dominant with a weak close.” Core compounders also saw notable weakness at 13.15%, indicating that selling pressure was not isolated to one part of the market. In contrast, “buyers active with a strong close” remained relatively limited across sectors, with just 5.78% of core compounders and 4.78% of cyclicals showing strong participation. This imbalance points to a session where gains at the index level were not fully supported by broad-based buying.

However, the session was far from outright bearish. The presence of balanced activity and selective strength across certain areas suggests that liquidity remains intact. Rather than a broad unwind, the market continues to exhibit characteristics of selective positioning, with capital rotating into specific themes rather than driving a unified move higher.

Sector-level performance reinforces this interpretation. Strength was concentrated in pockets of higher-growth and thematic areas, with AI and data-related names leading gains, while cybersecurity and cloud segments also showed resilience. Consumer tech and certain communication-driven segments posted modest advances, highlighting where buyers remain active.

At the same time, more traditional and economically sensitive areas struggled to keep pace. Transportation, infrastructure, and parts of the financial complex saw continued weakness, while defensive sectors such as healthcare and utilities failed to provide consistent support. This lack of cohesive leadership across major sectors suggests that the rally is not yet broad enough to signal a fully risk-on environment.

The divergence between strong index performance and mixed underlying participation reflects a market still navigating uncertainty. Much like recent sessions, macro conditions remain a key driver, with ongoing geopolitical developments, particularly around the Iran ceasefire, continuing to influence sentiment. Conflicting signals around the durability of the ceasefire are contributing to a cautious backdrop, limiting conviction despite positive price action.

In this context, yesterday’s move can be characterised as a selective rally rather than a broad-based advance. While headline indices moved higher, underlying market structure remains uneven, with sellers still active across multiple sectors and buyers concentrated in specific areas.

Looking ahead, the key question is whether buying participation can expand. A sustained increase in “buyers active with strong closes” across sectors would be needed to confirm a more durable uptrend. Until then, the market remains in a fragile state, where gains are possible but not yet fully supported by underlying breadth.