U.S. equities pushed to fresh record highs on Tuesday, but beneath the surface the session revealed a far more selective market than headline index performance suggested.

The S&P 500 closed at a new all-time high of 7,444.25, gaining 43.29 points (+0.58%) after trading between 7,375.13 and 7,460.04. The move was largely driven by continued strength in technology and semiconductor names, with investors once again leaning into AI infrastructure and mega-cap growth leadership.

The Nasdaq Composite led major indices higher, climbing 314.14 points (+1.20%) to close at 26,402.34, reinforcing that risk appetite returned aggressively to growth after the prior session’s defensive rotation. Alphabet and Tesla were among the major contributors as investors rotated back into high-beta technology exposure.

The Dow Jones Industrial Average lagged but still finished higher, gaining 57 points (+0.11%) to close at 49,760.56. Defensive heavyweights helped support the index, with gains from UnitedHealth Group, Walmart, and Coca-Cola offsetting weakness in Salesforce, IBM, and Caterpillar.

While the headlines looked broadly bullish, the internal market structure was more nuanced.

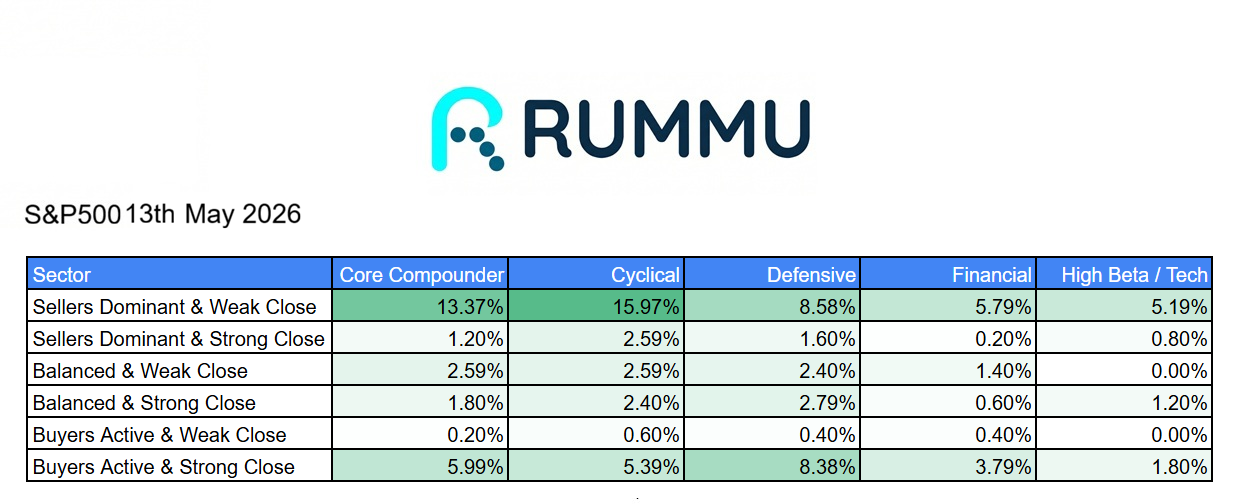

The S&P 500 sector rotation data showed meaningful weakness beneath the surface despite the record close. Core compounders saw 13.37% of stocks finish in seller-dominant weak closes, while cyclical stocks were even weaker at 15.97%. High-beta technology also showed limited broad participation, with only 1.8% of names finishing in buyers active and strong close territory.

That suggests the index rally was likely concentrated in a narrow group of large-cap technology leaders rather than broad participation across growth sectors.

Defensive sectors quietly showed stronger internal resilience.

Roughly 8.38% of defensive stocks finished with buyers active and strong closes, outperforming every major category. Financials also remained relatively stable with 3.79% of stocks finishing with strong closes.

This tells an important story.

Even as investors chased AI leaders higher, institutional money still maintained meaningful exposure to defensive sectors. That usually signals a market that remains bullish but cautious about broader economic uncertainty.

The Dow’s internal breadth painted an even clearer picture of this divergence.

Despite the index finishing green, 36.67% of Dow components closed in seller-dominant weak positions, while 43.33% finished with buyers active and strong closes.

That split reflects a highly rotational tape where capital aggressively moved between winners and losers throughout the day rather than broad market strength.

In simple terms, Tuesday was another record day for headline indices, but market breadth remains far less convincing than the index levels suggest.

Mega-cap technology continues doing most of the heavy lifting, defensive sectors remain quietly bid, and broader cyclical participation still looks fragile.

As long as AI leadership remains intact, indices can continue pushing higher.

But investors should continue watching breadth closely because record highs built on narrow leadership tend to become far more fragile if those leaders begin to fade.