Markets finished Monday with modest gains across major indices, but the underlying session was considerably weaker than the headline numbers suggest.

The S&P 500 closed at 7,412.84, up 0.19%, extending its move higher and briefly trading near another intraday high of 7,428.97 before fading into the close. The Dow Jones Industrial Average also gained 0.19% to finish at 49,704.47, while the Nasdaq Composite added just 0.10% to close at 26,274.13, despite hitting a fresh 52-week high during the session.

At the index level, it looked like another stable session with markets consolidating near record highs. Underneath the internals were far less constructive.

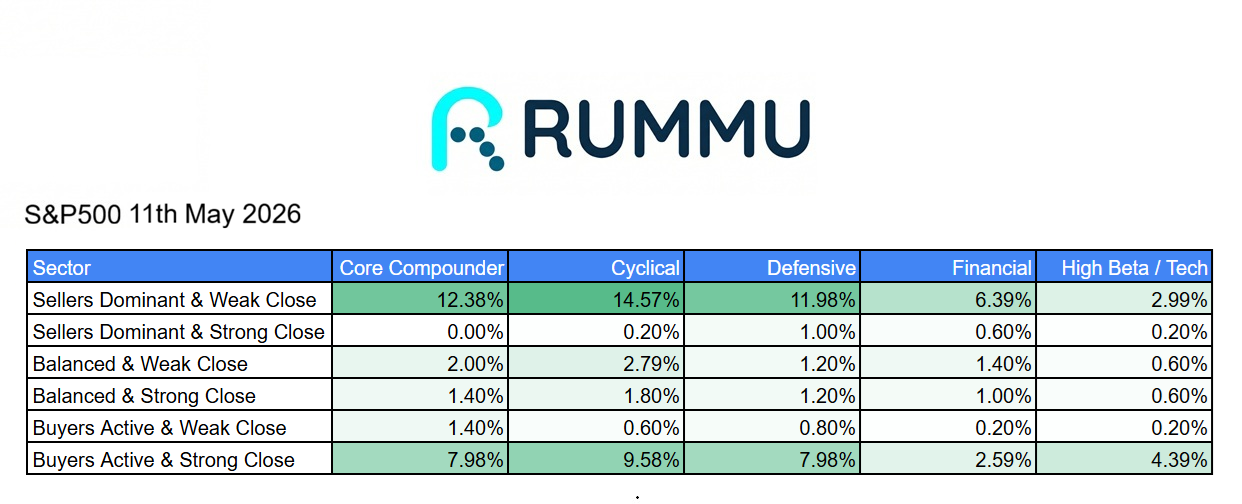

The intraday breadth data showed that 48.31% of stocks finished in sellers dominant with weak closes, compared with just 32.52% that closed in buyers active with strong closes.

While the indices managed to stay positive, nearly half of the market closed under meaningful selling pressure, suggesting the broader tape was much weaker than headline performance implied.

The largest area of weakness came from cyclicals, where 14.57% of names finished in sellers dominant with weak closes, followed by core compounders at 12.38% and defensives at 11.98%.

That broad selling pressure across multiple sectors suggests this was not simply isolated profit-taking. This is selective buying.

Financials were also relatively soft, with 6.39% of names closing under heavy selling pressure, while high beta technology remained comparatively resilient with 4.39% of stocks finishing in buyers active with strong closes.

That helps explain why the Nasdaq managed to remain positive despite broader weakness underneath the surface.

The sector heatmap reinforces how selective leadership has become.

Crypto and trading stocks surged 8.09%, making them one of the strongest groups of the day as investors rotated back into higher-risk speculative assets.

Materials technology jumped 6.90%, while automotive technology gained 5.41%, electronics rose 3.68%, and cloud SaaS added 3.09%.

Cloud infrastructure also remained strong, gaining 2.69%, while cybersecurity rose 2.02% and semiconductors advanced 1.76%.

That continued strength across infrastructure and selective growth segments remains one of the most consistent leadership trends in this market.

However, weakness was widespread elsewhere.

Biotech fell sharply by 8.95%, making it the weakest group of the session by a wide margin.

Healthcare services dropped 3.69%, internet services declined 3.64%, consumer finance fell 3.73%, and IT services dropped 2.32%.

Consumer technology also fell 2.69%, while healthcare equipment declined 2.85% and advertising declined 2.59%.

This level of dispersion matters.

The market continues moving higher at the index level, but leadership remains increasingly narrow and concentrated in specific momentum-driven groups.

That creates a more fragile structure beneath the surface.

The intraday price action also reflects that dynamic.

The S&P 500 spent much of the session trading higher before fading from intraday highs, while both the Dow and Nasdaq showed similar patterns of early strength followed by weaker momentum later in the day.

That typically signals some degree of profit taking as investors become more selective near elevated levels.

The broader takeaway is that headline index strength continues to mask increasingly fragmented internals.

The market is still making new highs, but participation is narrowing and a larger percentage of stocks are failing to hold gains into the close.

For now, strong performance in selective growth areas such as semiconductors, cloud infrastructure, crypto, and automation continues to support the indices. The question is for how long this can continue.