Markets traded with a mixed and fragile tone yesterday, reflecting a session where headline index moves masked a more uneven and rotational underlying structure.

Looking at the major indices, the divergence remains clear. The S&P 500 closed at 7,135.95, down just 0.04%, holding within a tight intraday range and suggesting relative stability at the index level. The Nasdaq Composite also remained broadly flat, rising 0.04% and continuing to hold near recent highs. In contrast, the Dow Jones declined more meaningfully, falling 0.57% and marking its fifth consecutive session of losses, highlighting continued pressure in more cyclical and industrial-heavy areas.

It reinforces the idea that while the broader market appears stable on the surface, underlying leadership remains narrow. Technology and growth-oriented segments continue to provide support, while cyclicals and more traditional sectors are struggling to gain traction.

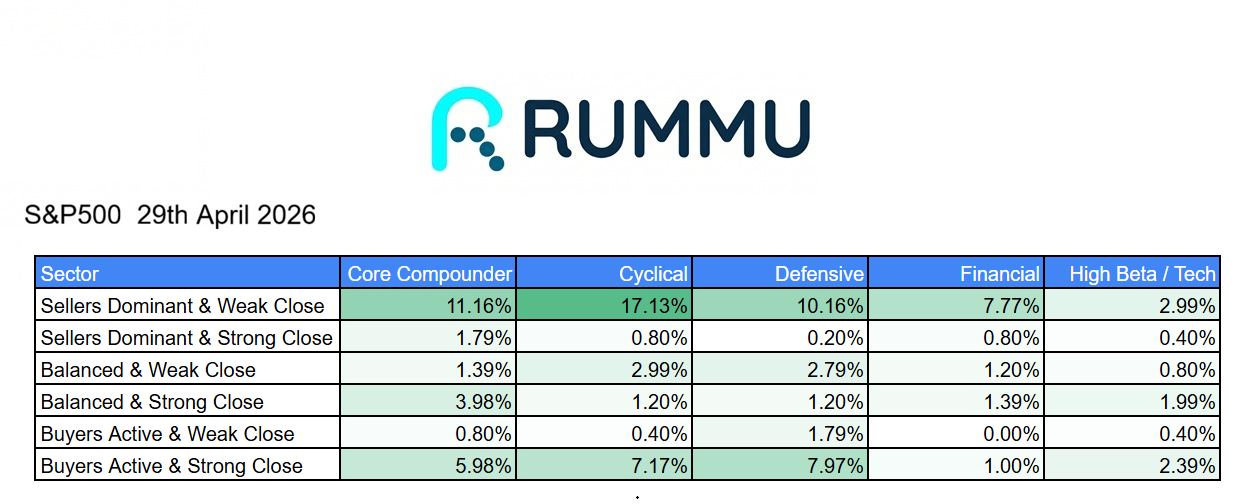

However, the underlying breadth data presents a more cautious picture.

Across sectors, selling pressure remained elevated, particularly within cyclicals where 17.13% of stocks were classified as “sellers dominant with a weak close.” Core compounders (11.16%) and defensives (10.16%) also saw meaningful selling activity, indicating that weakness was not isolated but spread across multiple areas of the market.

At the same time, buyer participation was present but not dominant. Buyers active with strong closes accounted for 7.17% in cyclicals, 7.97% in defensives, and 5.98% in core compounders. This suggests that while support remains, it is not yet broad enough to fully offset the selling pressure. This balance is telling.

It suggests the market is not undergoing a sharp de-risking, but rather a period of redistribution. Sellers have the upper hand in key areas, but buyers are still selectively stepping in, particularly into defensives and certain growth segments.

Sector performance reinforces this interpretation.

Strength was concentrated in specific areas, most notably cloud and infrastructure (+4.73%) and cloud / SaaS (+2.78%), alongside resilience in networking (+1.95%), marketplace (+1.84%), and agriculture (+1.74%). This cluster points to continued demand in digital infrastructure and platform-driven businesses, consistent with broader AI-related investment trends. At the same time, weakness remained widespread.

Healthcare technology (-4.51%) was the most notable laggard, followed by declines in crypto and trading (-2.96%), packaging (-2.73%), real estate services (-2.59%), and energy infrastructure (-2.50%). Telecom (-2.20%) and biotech (-2.20%) also underperformed, highlighting pressure across both defensive and higher-beta segments.

Unlike sessions where weakness is offset by clear rotation into defensives, yesterday’s price action reflects a market where leadership is narrow and uneven. Even traditionally defensive areas such as staples (-0.59%) and utilities (-0.18%) failed to provide consistent support.

Taken together, the data points to a market that is stabilising at the index level, but weakening beneath the surface.

The resilience in the S&P 500 and Nasdaq suggests that key leadership groups remain intact. However, the continued decline in the Dow and the breadth of sector-level weakness indicate that participation is narrowing and conviction remains selective.

In this context, the key question is whether this divergence can sustain.

If strength in technology and infrastructure-linked sectors continues to offset broader weakness, the market may remain stable despite uneven participation. However, if leadership begins to fade, the lack of broader support leaves the market more vulnerable to downside.

For now, the indices are holding near highs, but the underlying structure is becoming more fragile. The market is stable, but increasingly dependent on a narrowing set of leaders.