Markets traded with a weaker and more cautious tone yesterday, reflecting a session where headline index declines were supported by broad underlying selling pressure rather than isolated weakness.

Looking at the major indices, the move lower was consistent but varied in intensity. The S&P 500 closed at 7,138.80, down 0.49%, pulling back from recent highs within a relatively tight intraday range. The Nasdaq Composite led the decline, falling 0.90% and snapping its recent winning streak, while still holding near historic levels. In contrast, the Dow Jones was comparatively resilient, slipping just 0.05%, highlighting a degree of defensive stability beneath the surface.

It reinforces the idea that recent pressure is being driven primarily by higher-beta and technology segments, particularly following concerns around AI growth and profit-taking after a strong run. The Nasdaq’s sharper decline reflects this sensitivity, while the Dow’s relative stability points to continued support in more established, cash-generative names.

However, the underlying breadth data paints a more clearly negative picture.

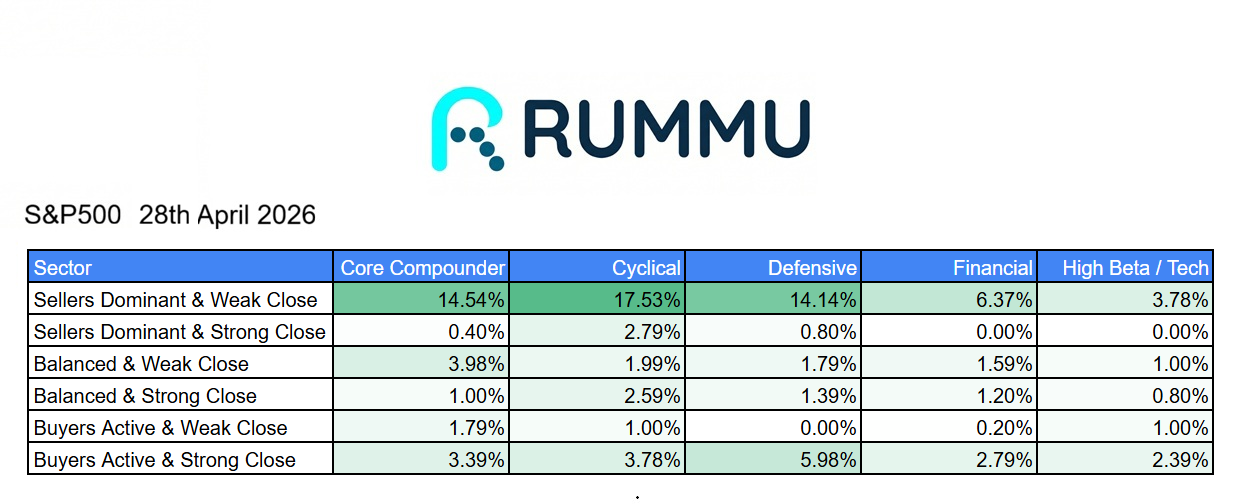

Across the market, 28.69% of stocks were classified as “sellers dominant with a weak close,” compared to just 42.83% showing “buyers active with a strong close” in prior sessions. Within sectors, selling pressure was particularly elevated in cyclicals (17.53%) and core compounders (14.54%), indicating that weakness was not confined to a single part of the market but spread across key leadership groups.

At the same time, buyer strength was notably limited. Only 3.39% of core compounders and 3.78% of cyclicals finished with “buyers active and strong closes,” suggesting that while some support remained, it lacked the scale needed to offset broader selling.

This shift in participation is telling.

It suggests that the session was not simply a pause or consolidation, but a more meaningful step back in momentum, particularly following recent highs. The presence of “sellers dominant with strong closes,” albeit smaller in percentage, also indicates that selling pressure persisted into the close rather than being absorbed intraday.

Sector performance reinforces this interpretation.

Weakness was visible across a wide range of areas, including healthcare technology (-3.61%), biotech (-3.38%), and healthcare services (-2.58%), alongside continued softness in cloud and infrastructure (-1.57%) and IT services (-1.63%). Consumer cyclicals and industrials also declined, highlighting the broad nature of the pullback.

At the same time, pockets of resilience did emerge.

Crypto and trading-related names (+2.05%), materials tech (+1.30%), and select areas of specialised technology (+0.92%) and energy infrastructure (+0.67%) showed relative strength. However, these gains were isolated and insufficient to shift the broader market tone.

This fragmentation is key.

Unlike sessions where weakness is offset by clear sector rotation, yesterday’s price action reflects a market where selling pressure was widespread, and leadership was limited. Even defensive areas such as staples (-0.26%) and utilities (-0.53%) failed to provide consistent support.

Taken together, the data points to a market that has moved from strength into a more cautious phase.

The recent rally, particularly in technology and AI-linked names, appears to be encountering resistance, with profit-taking now emerging as a more dominant force. While the pullback remains orderly, the breadth and sector dispersion suggest a loss of near-term momentum.

In this context, the key question is whether this represents a temporary reset or the beginning of a broader rotation.

If buyers begin to re-engage, particularly within core compounders and technology, the current weakness may prove to be a controlled consolidation. However, if selling pressure persists and spreads further, the market may move into a more sustained period of volatility.

The indices remain near highs, but the underlying participation has deteriorated, and leadership has narrowed.