Markets traded with a mixed but gradually improving tone, with recent price action highlighting a session where underlying strength was stronger than the headline index moves suggest.

Looking at the major indices, the divergence tells a consistent story. The Dow Jones Industrial Average closed at 49,167.79, down 0.13%, reflecting a relatively muted session at the index level. The move was contained within a tight range, with the majority of weakness occurring intraday rather than through sustained selling pressure. In contrast, the Nasdaq Composite continued to push higher, gaining 1.63% and testing record highs near 24,837, supported by ongoing strength in technology and growth-oriented names.

This divergence is important. It reinforces the idea that while broader markets remain stable, leadership continues to sit within higher-beta and technology segments, rather than being evenly distributed across indices.

However, the underlying breadth data presents a more constructive picture.

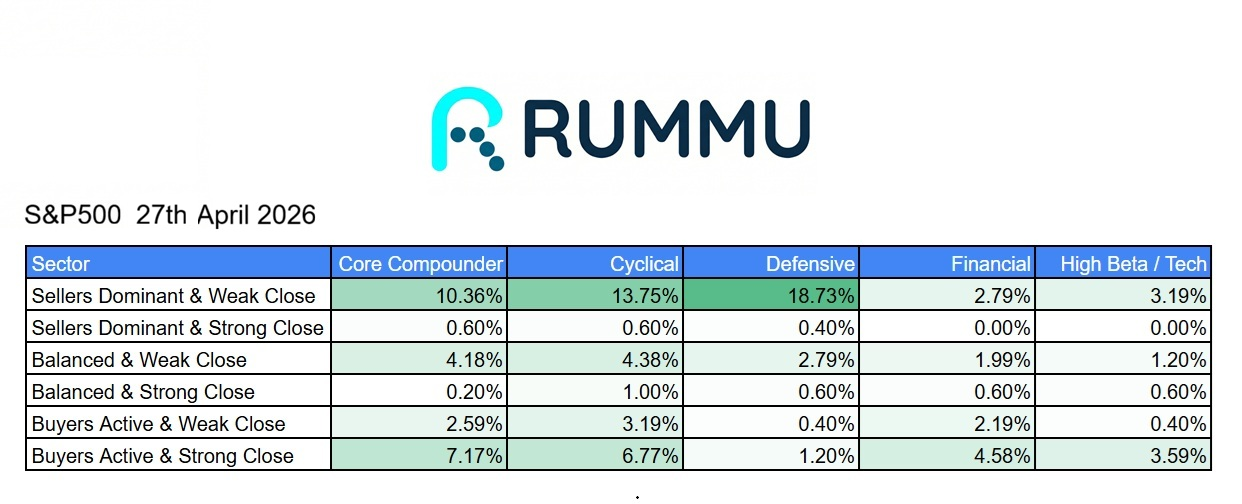

Across the S&P 500, 42.83% of stocks were classified as “buyers active with a strong close,” significantly outweighing the 28.69% of names that finished as “sellers dominant with a weak close.” This marks a notable shift from previous sessions, where selling pressure had been more dominant. Importantly, buyer strength was visible across multiple sectors, with core compounders (9.96%), cyclicals (10.16%), and defensives (9.56%) all showing meaningful participation.

This breadth improvement suggests that the session was not driven by narrow leadership alone. Instead, there was a broader base of buying activity supporting the market into the close.

The intraday structure reinforces this view.

The S&P 500 closed at 7,173.91, up 0.79%, with the session characterised by steady strength rather than sharp reversals. The index moved consistently higher from the open, with limited downside extension and a strong close relative to intraday levels. This type of price action is typically indicative of controlled accumulation rather than reactive buying.

Sector performance, however, remained mixed.

Strength was visible in areas such as cloud and SaaS (+2.52%), brokerage (+2.13%), and specialised technology (+1.70%), alongside resilience in financial infrastructure and banking. Automotive technology and consumer finance also contributed positively, indicating selective strength in cyclical and rate-sensitive segments.

At the same time, weakness persisted across other areas. Telecom (-2.34%), materials tech (-4.70%), and biotech (-3.81%) were among the laggards, while consumer defensive (-1.70%) and staples (-0.79%) also declined. This lack of uniformity suggests that while buyers are active, they remain highly selective in where capital is being deployed.

This fragmentation is key to understanding the current market structure.

The session does not reflect a broad-based risk-on move, but rather a selective expansion of buying interest, particularly within growth and technology-linked segments. Defensive areas failing to provide consistent support further reinforces that this is not a traditional rotation, but a more uneven re-engagement with risk.

Taken together, the data points to a market that is continuing to stabilise, with improving participation beneath the surface, but without fully aligned leadership.

The initial weakness seen in the Dow contrasts with the strength in the Nasdaq, while breadth data suggests that underlying demand is building. At the same time, sector dispersion remains elevated, indicating that conviction is still selective rather than broad.

In this context, the key question is whether this improvement in breadth can sustain.

If buyer participation continues to expand across sectors, it would suggest a more durable recovery is forming. However, if strength remains concentrated in technology and higher-beta names, the market may remain vulnerable to renewed volatility.

For now, the market appears to be moving toward a more constructive phase.

The selling pressure has eased, buyer activity is increasing, and the structure is gradually improving. But the recovery remains uneven, and leadership has yet to fully broaden.