Markets traded with a mixed and fragile tone yesterday, reflecting a session where early weakness was partially recovered before renewed selling pressure emerged into the afternoon. While headline index moves were relatively modest, the intraday structure and sector dispersion point to a market still struggling for clear direction.

The session began on a weak footing, with all major indices opening below the previous close, driven by ongoing macro uncertainty. The Dow Jones finished at 49,310.32, down 0.36%, while the S&P 500 declined 0.41% to 7,108.40. The Nasdaq Composite underperformed, falling 219 points, or 0.89%, to close at 24,438.50. Despite the early gap lower, markets showed signs of stabilisation through the morning, recovering a portion of losses before a sharp dip between 13:00 and 14:00 reversed momentum. From that point, indices failed to fully recover into the close, highlighting underlying fragility.

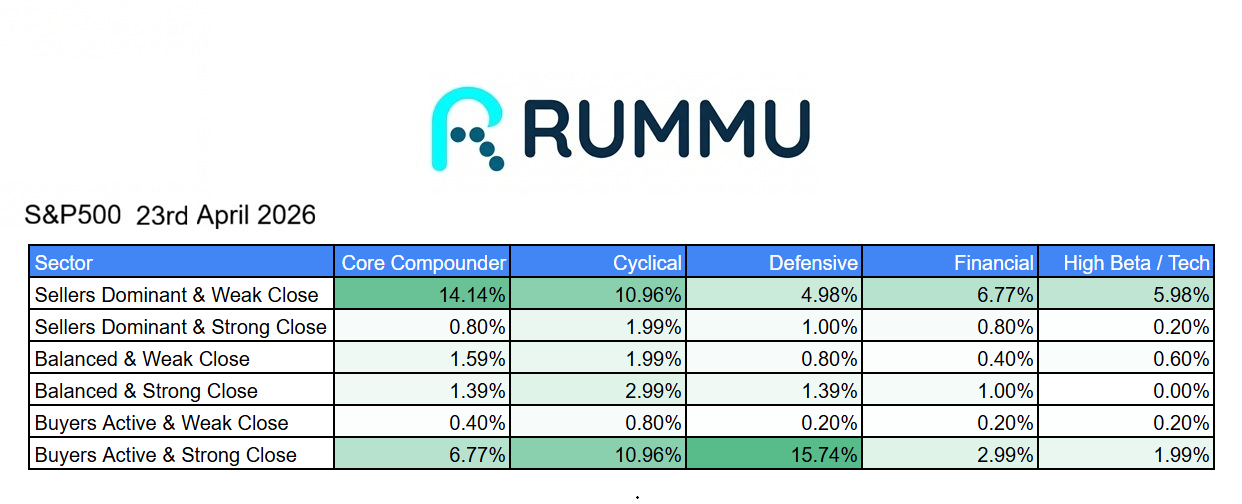

Breadth data presents a more constructive, but still nuanced, picture. While sellers remained active, particularly within core compounders where 14.14% of stocks were classified as “sellers dominant with a weak close,” there was also meaningful buyer participation. Defensive sectors showed the strongest closing strength, with 15.74% of names finishing as “buyers active with a strong close,” alongside 10.96% in cyclicals. This suggests that, unlike previous sessions dominated by distribution, buyers were willing to step in, particularly in areas offering stability and income.

However, this strength was not uniform.

Sector performance remained highly fragmented. Pockets of resilience were visible in utilities (+1.39%), energy infrastructure (+3.94%), and services-related segments, indicating selective rotation into more stable or infrastructure-linked areas. At the same time, weakness persisted across higher-beta and growth-oriented segments. AI and data-related names declined sharply, down 5.43%, while fintech (-2.60%), payments (-2.61%), and IT services (-3.04%) also remained under pressure. Healthcare services and biotech were among the weakest areas, falling over 5%, reinforcing the lack of consistent defensive leadership.

This divergence suggests that while buyers are present, they are highly selective. The market is not moving in a coordinated fashion, but rather rotating unevenly across sectors without establishing a clear leadership group.

Importantly, volatility remains contained. The VIX closed at 19.31, indicating a moderate volatility environment rather than a disorderly sell-off. This aligns with the broader price action, where declines are driven more by uncertainty and repositioning than outright risk aversion.

In this context, the session reflects a market in transition. The presence of both selling pressure and selective buying points to an environment where conviction remains limited. Gains are being challenged, but downside moves are not accelerating into panic.

Looking ahead, the key signal to watch is whether buyer strength continues to build, particularly in defensive and infrastructure-linked sectors. Sustained participation would suggest a stabilisation in market structure. However, if weakness in growth and high-beta areas persists without broader support, the market remains vulnerable to further downside.

For now, the setup remains balanced but fragile. The market is holding, but not yet convincingly recovering.