Markets retreated sharply on Tuesday as investors responded to rising geopolitical tensions in the Middle East and renewed concerns around energy prices. All three major U.S. indices finished lower, with the Dow Jones Industrial Average leading declines as risk appetite weakened throughout the session.

The S&P 500 fell 56.10 points, or 0.74%, to close at 7,553.68. The index traded in a relatively narrow range between 7,551.22 and 7,619.69 before finishing near the day’s lows, a sign that sellers maintained control into the close. Despite the decline, the benchmark remains less than 1% below its 52-week high, highlighting how resilient the broader uptrend has been in recent months.

The Dow Jones Industrial Average declined 620.72 points, or 1.21%, ending at 50,687.07. Meanwhile, the Nasdaq Composite lost 239.92 points, or 0.89%, closing at 26,853.98. The Nasdaq-100 outperformed slightly but still finished lower, falling 0.46% to 30,571.24 as weakness in several large-cap technology names weighed on sentiment.

The primary catalyst for the selloff was a combination of rising oil prices and escalating geopolitical tensions between the United States and Iran. Higher energy prices often create concerns about inflationary pressure and consumer spending, prompting investors to reduce exposure to more economically sensitive areas of the market.

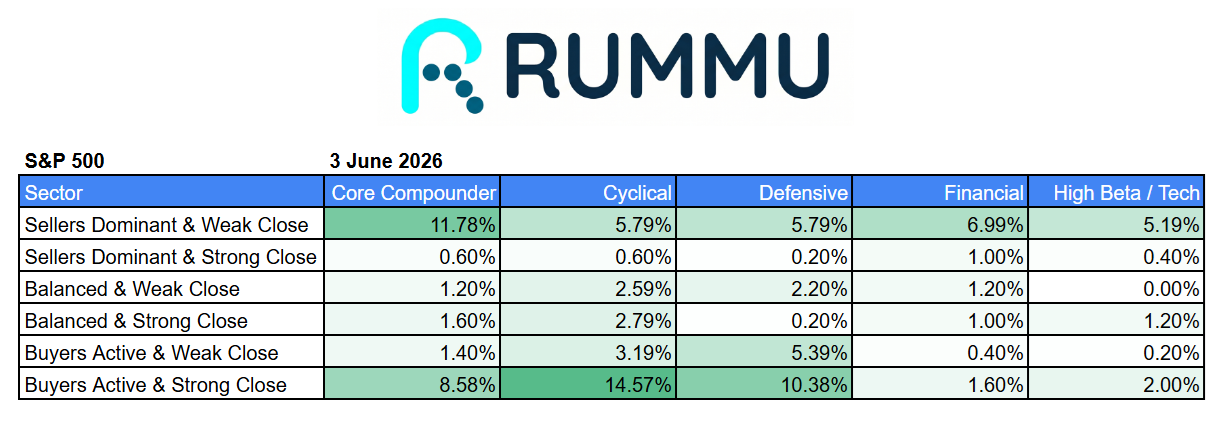

Market internals paint a more nuanced picture than the headline index declines suggest.

Within the Core Compounder category, 20.36% of stocks finished in either the “Sellers Dominant & Weak Close” or “Sellers Dominant & Strong Close” groups, while 9.98% managed to finish with buyers active into the close. This suggests that many high-quality growth and compounder names experienced broad selling pressure, although a meaningful group of stocks continued to attract demand despite the market weakness.

Cyclical stocks presented a more balanced picture. While 6.39% finished under seller dominance, 17.76% closed with active buyers, including 14.57% in the strongest accumulation category. This indicates investors were selective rather than indiscriminately risk-off, with some economically sensitive names continuing to attract capital despite the broader market decline.

Defensive sectors showed notable resilience. More than 15% of defensive stocks finished with buyers active, significantly outweighing those experiencing heavy selling pressure. This rotation toward defensive positioning is consistent with a market responding to geopolitical uncertainty and rising energy costs.

Financials displayed mixed behaviour. Seller-dominant stocks represented approximately 8% of the sector while only 2% finished with strong buying activity. This suggests investors remain cautious on financials as they assess the potential impact of higher energy prices and broader macroeconomic uncertainty.

Technology and higher-beta stocks were surprisingly orderly relative to the broader market narrative. While headlines focused on weakness in large-cap technology, only a small percentage of high-beta names experienced severe selling pressure, with many finishing in balanced trading categories rather than outright distribution. This suggests that the technology selloff was concentrated in specific large-cap names rather than a broad-based liquidation across the sector.

Perhaps the most important takeaway from the session is that the market weakness appeared driven more by macroeconomic and geopolitical concerns than by deteriorating corporate fundamentals. Defensive sectors attracted buyers, cyclical stocks showed pockets of strength, and many growth-oriented companies avoided the type of broad distribution typically seen during more significant market corrections.

For now, investors appear to be adjusting to geopolitical uncertainty rather than abandoning risk assets entirely. The coming sessions will likely depend on whether tensions in the Middle East continue to escalate and whether higher oil prices begin to materially influence inflation expectations and interest rate outlooks.