U.S. markets traded largely sideways on Wednesday as investors paused following the recent push to record highs, with the S&P 500 and Nasdaq finishing the session only marginally higher despite continued strength beneath the surface in cyclical sectors.

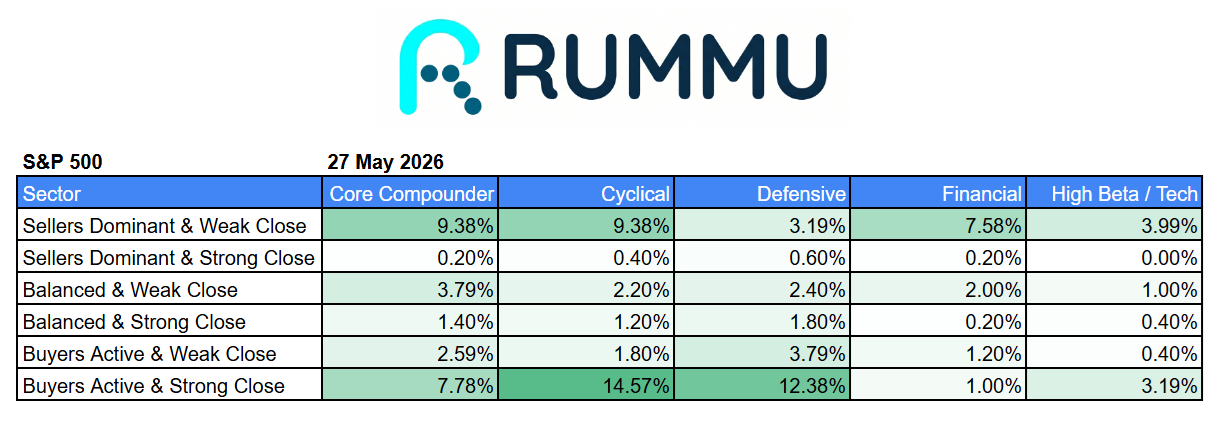

The S&P 500 closed at 7,520.36, gaining just 1.24 points, or 0.02%, after fluctuating between an intraday low of 7,499 and a high of 7,530. The muted index performance masked a more active internal rotation across sectors, with RUMMU intraday data showing cyclical and defensive groups continuing to attract strong buying interest into the close.

Cyclicals led the session internally, with 14.57% of cyclical stocks finishing in the “Buyers Active & Strong Close” category, the highest reading across the major sector groups. Defensive sectors also showed notable resilience, with 12.38% of defensive names registering strong closes despite broader index momentum slowing following recent all-time highs.

The Nasdaq Composite edged up 18.55 points, or 0.07%, to close at 26,674.73. Technology performance was more mixed compared to the previous session’s strong semiconductor-led rally, with several AI and infrastructure names seeing profit-taking while selective growth stocks continued to outperform.

Among the session’s strongest performers was AppLovin, which rallied 9.01% as investors continued rotating into higher-beta software and advertising technology names. Charles River Laboratories gained 4.19%, while Carvana climbed 3.91% as speculative growth appetite remained active beneath the surface. Aptiv and Albemarle also posted strong gains, reflecting continued investor interest in automotive technology and materials linked to long-term electrification themes.

On the downside, semiconductor and infrastructure-related names saw weakness after recent sharp advances. Analog Devices fell 3.83%, while Ciena declined 3.87% as networking and communications stocks paused following strong momentum in recent weeks. Constellation Energy lost 3.97%, and Boston Scientific dropped more than 5%, making it one of the session’s weakest large-cap performers.

The Dow Jones Industrial Average outperformed the broader market, rising 182.60 points, or 0.36%, to close at 50,644.28. Boeing, Procter & Gamble and Amazon helped support the index, while JPMorgan, Travelers and Chevron weighed on performance as financials and energy continued to show inconsistent participation.

RUMMU intraday market data highlighted a market that remains selective rather than broadly euphoric. Financials showed relatively weak buyer participation compared to cyclical and defensive sectors, while high-beta technology remained mixed despite the Nasdaq holding near record highs. Sellers continued dominating portions of core compounders and financial stocks, suggesting investors remain highly tactical beneath the surface rather than fully risk-on across all sectors.

The session reinforced the current structure of the 2026 market rally. Major indexes continue hovering near all-time highs, but leadership remains concentrated in specific pockets of cyclical growth, selective technology and momentum-driven stocks rather than broad-based participation across the entire market.