U.S. markets extended their recent pullback on May 19 as rising macro uncertainty and fading momentum in cyclical sectors weighed on investor sentiment, with all three major indexes closing lower in a broad-based risk-off session.

The S&P 500 fell 49.44 points, or 0.67%, to close at 7,353.61 after trading in a range of 7,333.68 to 7,395.32. The Dow Jones Industrial Average declined 322.24 points, or 0.65%, to finish at 49,363.88, while the Nasdaq Composite led losses, falling 220.02 points, or 0.84%, to close at 25,870.71 as weakness in growth and technology continued to pressure broader sentiment.

Within the Dow, defensive names provided some stability, with Verizon and Amgen leading gains, while Cisco, Boeing and 3M weighed most heavily on the index as industrial and technology names saw profit-taking after recent strength.

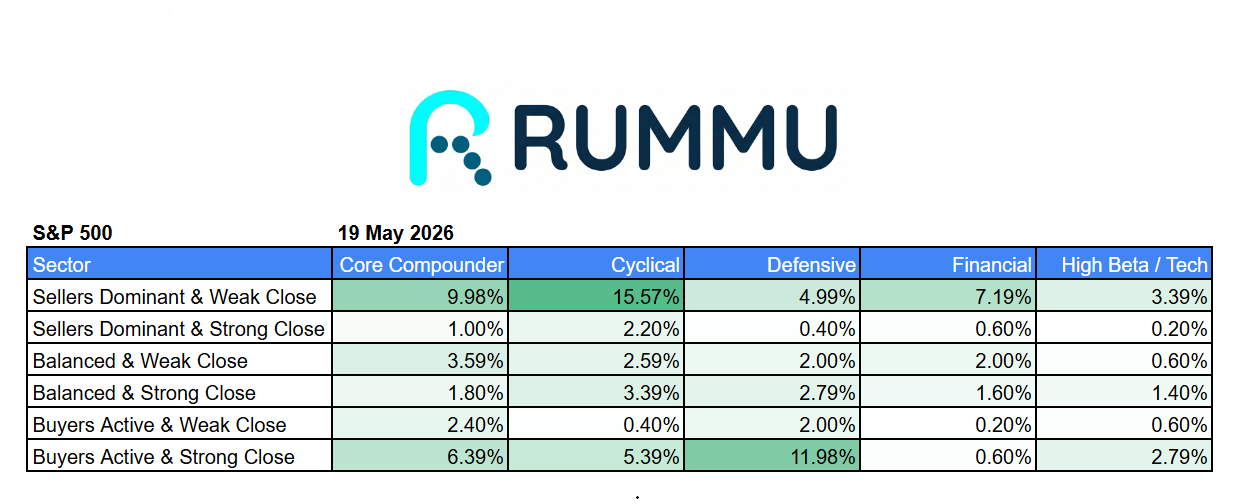

The sector breadth data reveals a market that was far weaker beneath the surface than the headline indexes alone suggest.

Cyclical stocks saw the heaviest selling pressure, with 15.57% of names closing in the “seller dominant and weak close” category, while only 5.39% managed to finish with active buyers in control. This points to a clear rotation away from economically sensitive sectors as institutional money reduced exposure into the close.

Core compounders also weakened, with seller-dominant weak closes at 9.98% versus just 6.39% of stocks showing strong buyer participation. That suggests even high-quality growth names were not immune to broader market pressure.

Defensive sectors stood out as the relative area of strength. Nearly 12% of defensive stocks finished in the “buyers active and strong close” category, significantly outweighing the 4.99% in seller-dominant weak closes. This is a classic sign of capital rotating toward earnings stability and lower volatility rather than exiting equities entirely.

Financials looked particularly fragile, with very little meaningful buying support into the close. Just 0.60% of stocks finished in the strongest buyer category, while 7.19% closed under clear seller dominance, reinforcing signs that investors remain cautious around rate-sensitive businesses.

High beta and technology names also remained under pressure, with buyer conviction fading after a strong leadership run earlier in the month.

The broader message from Monday’s session is that this was not simply a mild market decline. It looked more like a continuation of internal rotation, with capital moving away from cyclical and higher-beta areas while defensive sectors absorbed relative inflows.

Markets now appear caught between resilient economic fundamentals and growing pressure from higher yields, inflation concerns and stretched valuations in leadership sectors. For now, institutional positioning suggests investors are becoming more selective rather than broadly bearish, but the defensive tilt in breadth data points to a market becoming increasingly cautious beneath the surface.