U.S. markets delivered a mixed session Monday as investors balanced rising Treasury yields against continued strength in selective areas of the economy, with defensive industrial names helping stabilize the broader market while technology remained under pressure.

The S&P 500 finished almost flat, slipping just 5.45 points to close at 7,403.05, down 0.07% on the session. Despite the muted headline move, the index experienced notable intraday volatility, trading between 7,353.17 and 7,434.06 as markets attempted to recover from Friday’s sharp pullback.

The Dow Jones Industrial Average outperformed, rising 159.95 points or 0.32% to close at 49,686.12. Gains in industrial and energy names helped support the index, with 3M jumping 4.32%, Salesforce climbing 3.38% and Chevron gaining 2.57%.

Meanwhile, the Nasdaq Composite continued to lag as higher Treasury yields pressured growth valuations. The index fell 134.41 points or 0.51% to close at 26,090.73, with semiconductor weakness weighing heavily on sentiment. NVIDIA declined 1.39% as investors continued rotating away from some of the market’s strongest momentum trades.

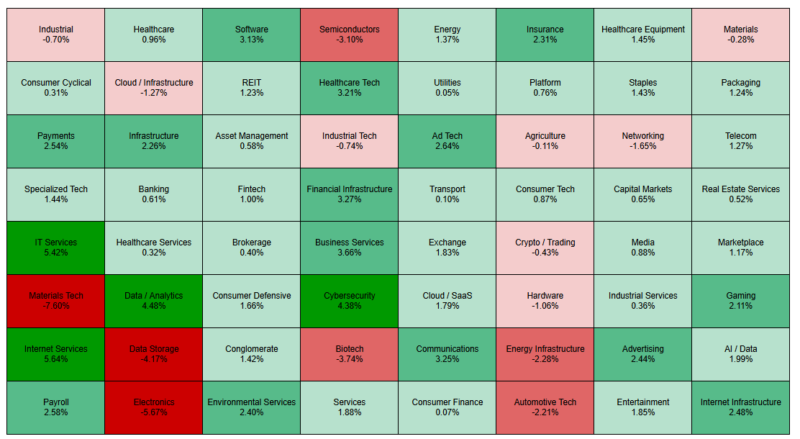

The sector heatmap showed a market that remained highly selective rather than broadly risk-off.

Software led the stronger areas of the market, gaining 3.13%, while cybersecurity rose 4.38%, data and analytics climbed 4.48% and internet services surged 5.64%. IT services also stood out with a sharp 5.42% gain, suggesting investors are still actively deploying capital into profitable digital infrastructure and enterprise software businesses despite broader technology weakness.

At the same time, semiconductors fell 3.10%, materials technology dropped 7.60% and electronics declined 5.67%, highlighting continued pressure on hardware and manufacturing-related areas tied closely to the AI infrastructure trade.

Interestingly, financial infrastructure and business services remained strong, rising 3.27% and 3.66% respectively, while insurance stocks gained 2.31%, suggesting investors continue favoring businesses with recurring cash flow and stable earnings visibility.

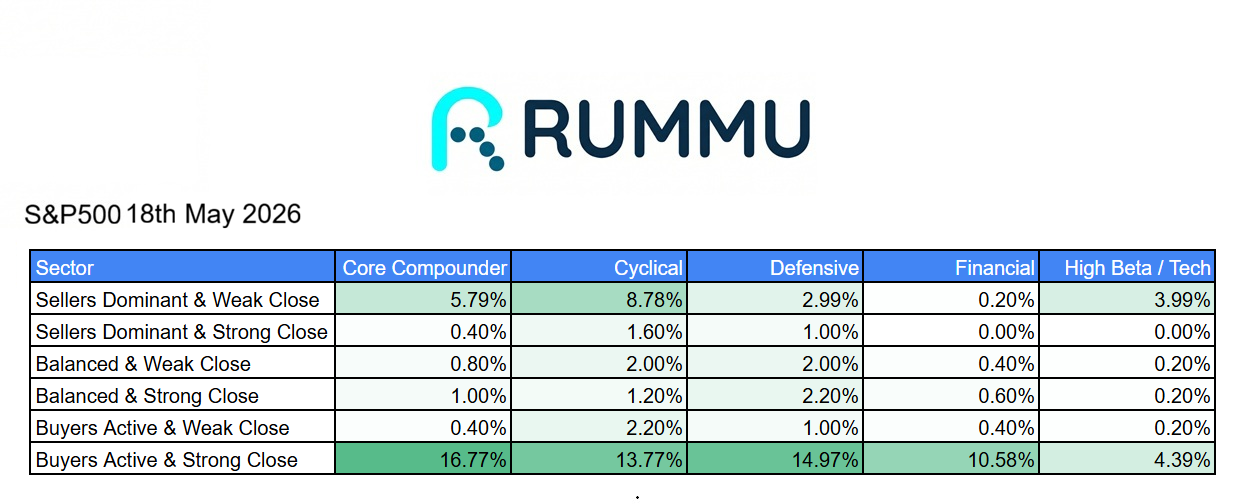

intraday breadth data painted a surprisingly constructive picture beneath the surface. Core compounders saw 16.77% of stocks close in the “buyers active and strong close” category, far outweighing the 5.79% classified as “seller dominant and weak close.” Defensive sectors also held up relatively well, with nearly 15% of stocks finishing with active buyer participation into the close.

That suggests institutional money may still be selectively accumulating quality businesses even as broader indexes consolidate.

The weakest area remained higher-beta speculative assets, where momentum continued fading after the recent rally. Crypto trading names, semiconductor hardware and automotive technology all struggled as rising bond yields forced investors to reassess risk appetite.

The broader market now appears caught between two competing narratives.

On one side, higher Treasury yields and persistent inflation concerns continue pressuring valuation multiples, particularly in growth and AI-related hardware stocks. On the other, underlying breadth across software, cybersecurity, business services and quality compounders suggests institutional investors are still willing to buy durable earnings streams on weakness.

For now, the market does not appear to be breaking down structurally. Instead, it looks increasingly like a rotational environment where capital is moving aggressively beneath the surface rather than exiting equities entirely.