U.S. equities paused for breath on Tuesday after an explosive rally pushed major indices to fresh highs earlier in the week, with investors rotating out of high-beta growth names and into more defensive sectors as markets digested recent gains.

The S&P 500 slipped 11.88 points, or 0.16%, to close at 7,400.96 after reaching an intraday high of 7,409.57. That came just one session after the index closed at a record 7,412.84 on Monday and briefly pushed toward another all-time high before sellers stepped in. The day’s trading range between 7,338.54 and 7,409.57 reflected a market that spent much of the session consolidating rather than aggressively selling off.

This did not feel like the start of a broader risk-off move. It looked far more like investors taking profits after a powerful AI-driven rally that has pushed valuations sharply higher in recent sessions.

The Nasdaq Composite saw the largest pullback among major indices, falling 185.92 points, or 0.71%, to close at 26,088.20. After touching a recent 52-week high of 26,359.31 on Monday, technology shares faced the heaviest selling pressure as traders rotated away from momentum names that had led the recent breakout.

The Dow Jones Industrial Average moved in the opposite direction, rising 56.09 points, or 0.11%, to close at 49,760.56. The relatively stronger Dow performance reflected growing investor preference for more defensive large-cap names over speculative growth exposure.

That rotation was visible beneath the surface of the market.

Defensive sectors clearly outperformed throughout the session. Healthcare rose 1.31%, healthcare equipment gained 1.07%, utilities climbed 0.59%, staples added 0.23%, and insurance advanced 0.33%.

Biotech was one of the strongest performing groups on the day, rising 1.97%, while brokerage stocks gained 1.52%, networking added 1.15%, marketplace stocks rose 1.17%, and advertising climbed 1.21%.

Electronics stood out as the strongest sector overall, surging 4.84%, likely driven by continued enthusiasm tied to semiconductor and AI supply chain demand.

On the other side of the market, software fell 2.36%, IT services dropped 3.69%, materials technology declined 2.99%, crypto trading names fell 2.01%, hardware dropped 1.80%, consumer tech lost 1.43%, and internet services declined 1.71%.

Investors were selectively reducing exposure to crowded technology trades while reallocating capital toward more stable earnings sectors that tend to perform better during periods of market consolidation.

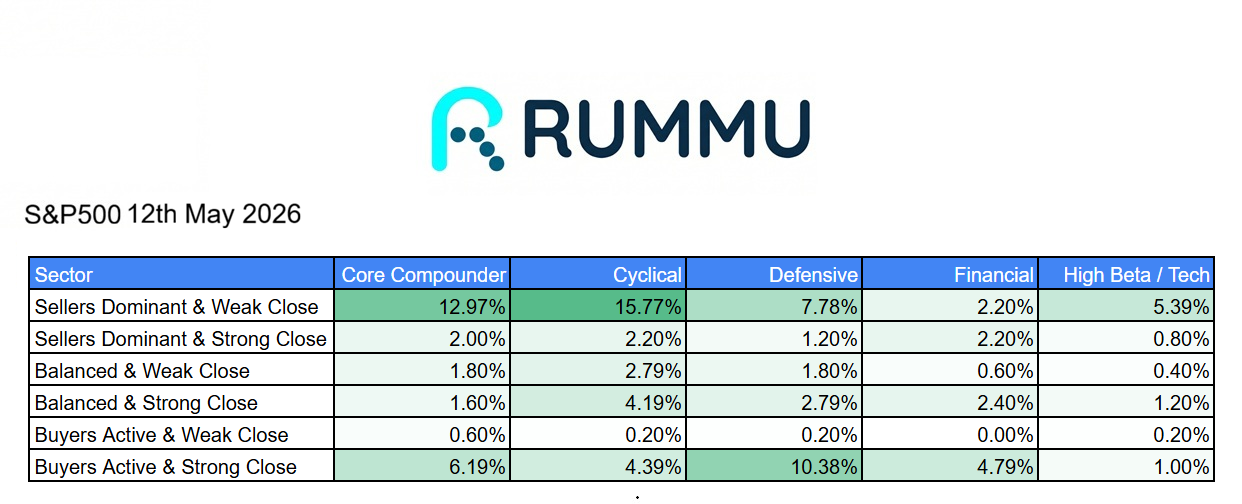

Market breadth data reinforced that view.

In cyclical sectors, 15.77% of stocks finished in the “sellers dominant and weak close” category, showing meaningful weakness into the close. Core compounders also saw elevated selling pressure, with 12.97% closing weak.

Meanwhile, defensive stocks showed the strongest late-session buying activity. Roughly 10.38% of defensive names finished in the “buyers active and strong close” category, significantly outperforming every other market segment. Financials also showed improving demand, with 4.79% of stocks finishing with strong closes.

That closing behavior suggests institutions were actively repositioning rather than simply exiting equities altogether.

The market remains near record highs, but Tuesday’s action highlighted growing caution around stretched growth valuations after the recent rally.

For now, the broader trend remains intact.

The S&P 500 is still trading near all-time highs. The Dow continues showing relative strength. The Nasdaq remains the leadership index despite short-term weakness.

Tuesday looked less like a breakdown and more like a healthy reset, with investors rotating into defense while waiting to see whether the next leg higher can be supported by earnings growth rather than pure momentum.