Markets delivered a strong follow-through session on Wednesday, with broad indices pushing to fresh highs as sentiment improved meaningfully on the back of easing geopolitical concerns and continued strength in technology.

The S&P 500 rose 1.46% to close at 7,365.12, marking another record high and finishing near the top of its intraday range after opening at 7,294.14. The session showed steady strength throughout the day, with limited pullbacks and a close near highs, which typically reflects sustained institutional demand rather than short-term trading activity.

The Nasdaq led once again, gaining 2.02% to 25,838.94, also closing at a record high, supported by continued momentum in AI-linked technology names. Meanwhile, the Dow Jones Industrial Average advanced 1.24% to 49,910.59, briefly reclaiming the 50,000 level intraday before closing just below it.

At the headline level, this was a clear risk-on session.

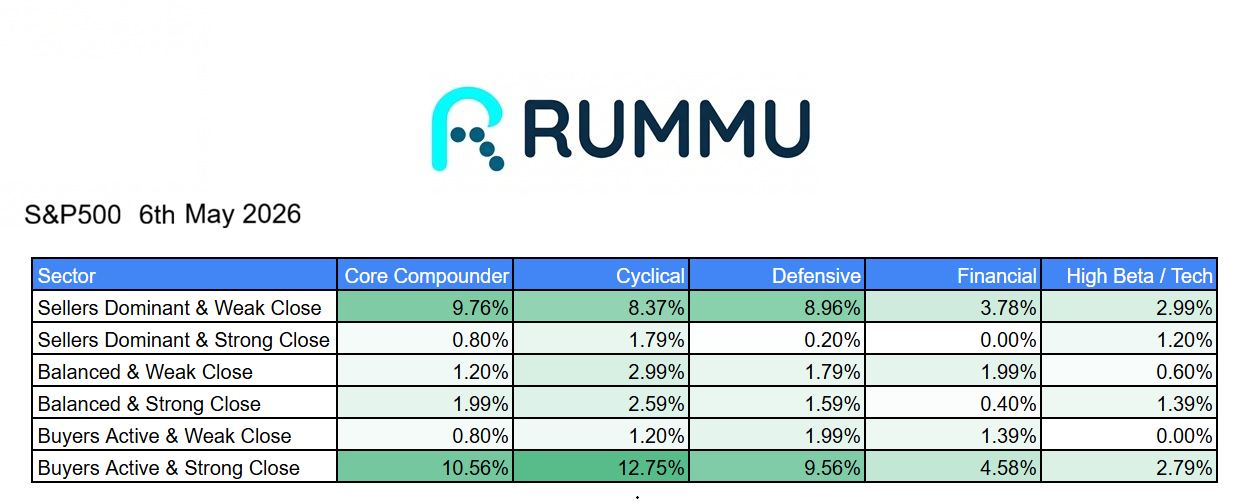

The intraday breadth data showed that 40.27% of stocks finished in buyers active with a strong close territory, compared with 32.86% in sellers dominant with weak closes. That represents a positive skew toward buyers, but not an overwhelming surge in participation.

The strongest participation came from cyclicals, where 12.75% of names closed with strong buyer control, suggesting investors were willing to re-engage with economically sensitive areas following recent volatility. Core compounders also showed solid participation at 10.56%, while defensives came in at 9.56%, indicating a reasonably balanced recovery across sectors.

Financials lagged somewhat in terms of conviction, with only 4.58% of names finishing in buyers active strong close territory, which helps explain why the Dow, while strong, did not fully break out in the same way as the Nasdaq.

Technology participation was more nuanced.

Despite the Nasdaq’s strong performance, only 2.79% of high beta technology names finished in buyers active strong close territory, suggesting that leadership remained concentrated in a relatively small group of large-cap names rather than broad-based participation across the entire sector.

The industry-level data reinforces that point.

Leadership was highly concentrated in infrastructure and hardware-linked areas. Hardware rose 4.44%, one of the strongest performing groups of the session, while cloud infrastructure gained 3.57% and automotive technology added 3.23%. Semiconductors also contributed positively with a 1.86% gain.

This aligns closely with continued strength in AI infrastructure and enterprise spending themes.

At the same time, there was clear weakness across parts of the software and services ecosystem. IT services fell 5.62%, materials technology declined 4.12%, and ad tech dropped 2.69%, highlighting that not all technology segments participated in the rally.

Healthcare services also saw notable pressure, declining 2.54%, while healthcare technology fell 1.91%, suggesting some defensive rotation out of certain areas.

Interestingly, biotech was one of the stronger performers, rising 3.57%, indicating selective rotation within healthcare rather than broad sector weakness.

Financial-linked industries were mixed.

Capital markets rose 0.68% and banking gained 0.14%, but financial infrastructure declined 1.57%, showing that participation in financials was uneven and lacked strong conviction.

Consumer-facing areas were relatively stable.

Consumer technology rose 1.34%, while staples were flat and consumer cyclicals posted only modest gains, suggesting that while sentiment improved, it did not translate into aggressive broad consumer positioning.

The overall takeaway from the session is that the market remains in a strong uptrend, but leadership continues to be concentrated.

The rally was driven by a combination of improving geopolitical sentiment, continued AI-driven optimism, and supportive earnings momentum. The fact that indices closed near session highs reinforces that buyers were in control throughout the day.

However, participation remains selective.

The strongest gains continue to come from infrastructure, hardware, and AI-linked segments, while other areas of the market are either lagging or showing outright weakness…For now, that is enough to push indices higher.