U.S. equities suffered their sharpest decline in weeks on Friday as investors aggressively reduced exposure to technology, AI-related businesses and higher-growth sectors. The selloff was broad enough to pull all major indices lower, but the damage was concentrated in the areas that have led the market higher throughout much of 2026.

The S&P 500 fell 200.57 points, or 2.64%, closing at 7,383.74. After opening at 7,537.36, the index briefly traded near session highs before selling pressure accelerated throughout the day, pushing the market to an intraday low of 7,368.63.

The Nasdaq bore the brunt of the decline, dropping 4.18% as investors aggressively exited technology and AI-related positions. The Dow Jones Industrial Average proved relatively resilient but still lost 1.35%, highlighting that risk aversion spread well beyond technology stocks.

The sector heatmap paints a clear picture of where the selling pressure was concentrated and Technology takes the hit

Semiconductors led the decline, falling 6.11%, while Materials Technology dropped 6.23%. Data Storage fell 5.38%, Cloud & Infrastructure lost 5.23%, Electronics declined 4.89%, and Ad Tech dropped 4.61%.

Several other technology-related segments also experienced significant weakness:

- Networking: -4.12%

- Hardware: -4.03%

- Crypto & Trading: -3.97%

- AI / Data: -3.41%

- Fintech: -3.02%

- Software: -2.82%

The scale of these declines suggests investors were reducing exposure to many of the market’s highest-performing themes rather than reacting to company-specific news.

Defensive rotation emerges: While most sectors finished lower, several traditionally defensive areas attracted buyers.

Insurance gained 2.04%, Consumer Defensive stocks rose 1.01%, Staples advanced 1.66%, Utilities added 1.29%, and REITs climbed 1.24%.

These gains indicate that capital was not simply leaving equities altogether. Instead, investors were rotating away from growth-oriented sectors and seeking shelter in businesses with more stable earnings profiles.

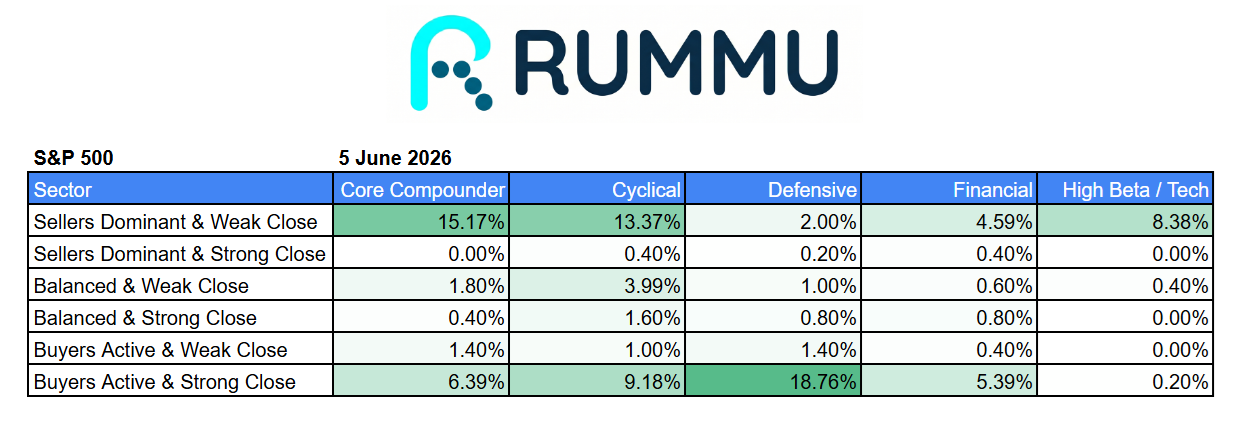

RUMMU’s intraday market behaviour data highlighted one of the most interesting aspects of the session.

Despite the sharp decline in major indices, Defensive stocks recorded the strongest buyer participation of any sector group. An impressive 18.76% of Defensive names finished the day in the “Buyers Active & Strong Close” category.

By contrast:

- Core Compounders recorded 15.17% of stocks in “Sellers Dominant & Weak Close”

- Cyclicals recorded 13.37%

- High Beta / Tech recorded 8.38%

The data suggests this was not a market-wide panic. Instead, it was a decisive sector rotation.

Investors were actively selling growth, technology and cyclical names while simultaneously accumulating defensive businesses.

Broadening correction or healthy rotation?

The key question for investors is whether Friday’s move represents the beginning of a deeper correction or simply a reset after an extended rally.

Several signs point toward the latter.

Defensive sectors remained healthy. Financials showed relatively balanced behaviour. Market participation did not collapse across every area simultaneously.

Instead, the market appears to be reassessing valuation and expectations within technology and AI-related industries after an extraordinary run higher throughout 2026.

The sectors experiencing the largest declines were also among the strongest performers year-to-date, suggesting profit-taking may have played a significant role.

Friday’s session serves as a reminder that leadership changes can occur quickly in highly valued markets.

Technology, semiconductors and AI infrastructure have driven much of the market’s gains this year, but the sharp reversal demonstrates that investors remain sensitive to valuation, expectations and positioning.

The encouraging sign is that money did not leave the market entirely. Instead, it flowed toward defensive sectors, insurance, utilities and consumer staples.

For now, the market appears to be experiencing a rotation rather than a collapse. Whether this develops into a broader correction or simply a temporary pause in the AI-driven rally will likely depend on upcoming economic data, earnings revisions and investor appetite for risk heading into the summer months.

One thing is clear: Friday marked the most significant shift away from growth and toward defence seen in several months.