U.S. equities staged a modest recovery on Monday following Friday’s sharp selloff, although the rebound lacked conviction beneath the surface. Investors cautiously returned to technology and semiconductor stocks after one of the weakest sessions of 2026, helping lift the S&P 500 and Nasdaq, while the Dow Jones Industrial Average slipped slightly lower.

The S&P 500 gained 21.99 points, or 0.30%, to close at 7,405.73. The index opened strongly at 7,440.57 and climbed to an intraday high of 7,466.81 before sellers gradually emerged throughout the session, pushing the market close to its daily low of 7,395.13 by the close. While the positive finish was encouraging, the inability to hold early gains suggests investors remain cautious following last week’s volatility.

The Nasdaq Composite led the major indices higher, rising approximately 0.86% as buyers returned to technology and semiconductor shares. The recovery comes after Friday’s heavy AI-driven selloff and suggests investors are not yet ready to abandon the sector despite growing concerns around valuations and earnings expectations.

The Dow Jones Industrial Average was the notable laggard, falling 80.77 points, or 0.16%, to finish at 50,786.01. Dow components traded within a wide range between 50,732 and 51,277 before ultimately closing in negative territory.

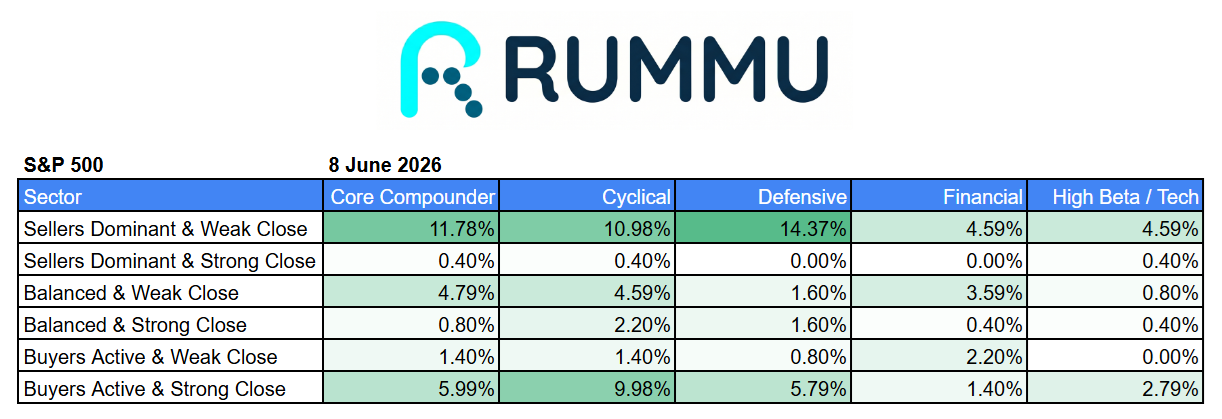

Intraday Data Shows Sellers Still In Control

RUMMU’s intraday market behaviour data paints a more cautious picture than the headline index gains suggest.

Across every major sector group, seller-dominated stocks continued to outnumber strong buyer closes. Core Compounders saw nearly 12% of stocks finish in the “Sellers Dominant & Weak Close” category compared with just 6% ending with strong buyer participation. Cyclicals showed a similar pattern, with 10.98% finishing under seller control versus 9.98% recording strong buyer closes.

Defensive sectors were particularly weak beneath the surface. More than 14% of defensive stocks finished with seller-dominated weak closes, while only 5.79% recorded strong buyer participation. This suggests investors were rotating away from traditional safe havens after last week’s risk-off move.

Financials remained relatively balanced, although buying enthusiasm was noticeably weaker than during last week’s healthcare and banking-led rally.

The takeaway is that Monday’s gains were driven more by a rebound in select technology names than broad market strength.

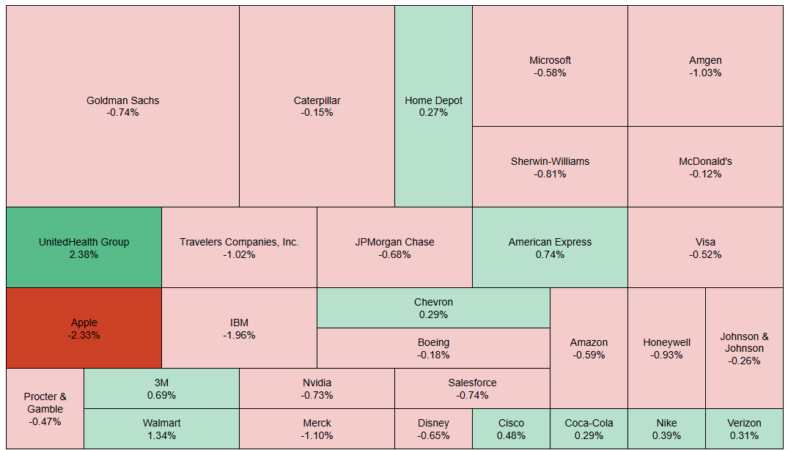

Dow Heatmap Highlights Mixed Leadership

The Dow Jones heatmap reinforced the market’s uneven nature.

UnitedHealth was the standout performer, gaining 2.38% and continuing its recovery after recent volatility. Walmart added 1.34%, while American Express gained 0.74%. Smaller gains from Chevron, Home Depot, Cisco, Coca-Cola and Verizon helped offset broader weakness.

However, several heavyweight constituents remained under pressure.

Apple fell 2.33%, making it one of the weakest performers in the index. IBM lost 1.96%, Merck declined 1.10%, and Travelers, Amgen and Honeywell also closed lower. Even market leaders such as Microsoft, Amazon, Visa and Goldman Sachs finished the session in negative territory.

This broad distribution of small losses across many large-cap names explains why the Dow struggled despite strength in a handful of sectors.

A Technical Bounce, Not Yet a Full Recovery

The most important theme from Monday’s session was stabilization.

After Friday’s aggressive selloff, investors stepped back into technology and semiconductors, helping the Nasdaq outperform. However, the intraday data suggests conviction remains limited. Selling pressure is still present across many sectors, and defensive stocks that previously attracted buyers are now showing signs of distribution.

Markets often experience short-term rebounds following large declines, particularly when positioning becomes stretched. Whether Monday’s gains mark the beginning of a sustained recovery or merely a temporary bounce will depend on how technology shares perform over the coming sessions.

For now, investors appear willing to buy the dip in AI and semiconductor stocks, but the broader market is still searching for direction. The S&P 500 managed a positive close, yet RUMMU’s underlying data suggests caution remains the dominant sentiment beneath the surface.